Vietnam’s energy narrative is entering a second, more structurally consequential chapter. The first chapter — a rapid expansion of onshore solar and wind driven by feed-in tariffs — deployed more than 24 GW of renewable capacity in just a few years and briefly made Vietnam one of the top solar markets in the Asia-Pacific region. That growth was fast and, at times, disorderly. Grid infrastructure did not keep pace with generation, curtailment became a recurring problem, and Vietnam Electricity (EVN) accumulated over USD 1 billion in losses in 2023 as retail prices failed to cover rising power purchase costs.

The second chapter is more deliberately institutional. The Revised Power Development Plan VIII (PDP8R), approved in April 2025, sets targets that would require Vietnam to roughly double its installed capacity by 2030 and commit USD 136 billion to generation and transmission investment over the 2026–2030 period alone. Offshore wind, which today has zero commercial-scale capacity, is assigned a central role. The policy question is no longer whether Vietnam will transition its energy system, but whether the regulatory and financing frameworks can convert ambitious targets into bankable projects at the scale and pace that demand growth requires.

The Scale of Vietnam’s Electricity Demand Challenge

A System Under Structural Pressure

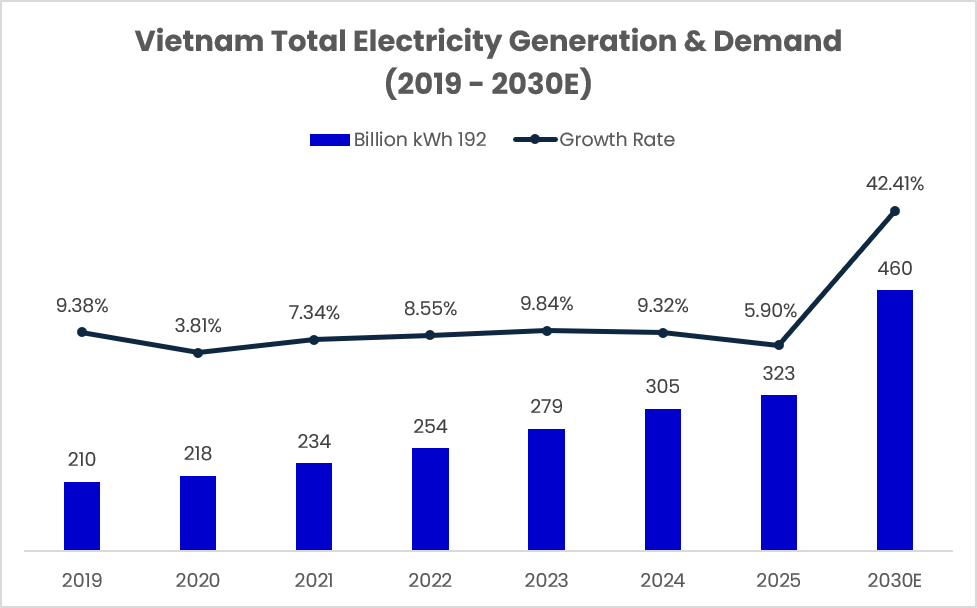

Vietnam’s power system has grown substantially. Total installed capacity reached approximately 90 GW by the end of 2025, making it the largest power grid in Southeast Asia by installed base and ranking among the top 20 globally. Yet this position reflects growth from a relatively low base rather than a system already configured for the decade ahead. Annual electricity demand is growing at approximately 7.2% per year according to BMI Research projections through 2034, driven by manufacturing expansion, rising household income, and the digitalisation of industry and services.

Total electricity generation reached an estimated 323 billion kWh in 2025, up from 192 billion kWh in 2018. At the projected growth rate, the system will need to deliver approximately 460 billion kWh by 2030 — an increase of more than 40% over the current base within five years. This is the fundamental pressure driving the scale of Vietnam’s investment programme: not a transition away from one energy source in the abstract, but the need to add sufficient reliable capacity to keep pace with one of the fastest-growing electricity demand profiles in Southeast Asia.

Figure 1: Vietnam’s electricity generation has grown from 192 billion kWh in 2018 to an estimated 323 billion kWh in 2025. At the 7.2% annual demand growth rate projected by BMI Research, the system must deliver approximately 460 billion kWh by 2030. Source: EVN / BMI Research.

At that growth rate, Vietnam needs to add not just capacity but the right kind of capacity. The coal-heavy existing mix — which still accounts for around 32.7% of installed capacity — creates both environmental and energy-security constraints. Gas-fired power, which many planners viewed as the transition bridge, has faced slow progress on LNG import infrastructure. This leaves renewable energy, particularly solar, wind, and storage, as the principal avenue for new capacity, and the Revised PDP8 formalises that direction.

The Existing Power Mix and What It Reveals

Coal Dominance, Hydropower Limits, and a Fast-Growing Renewables Base

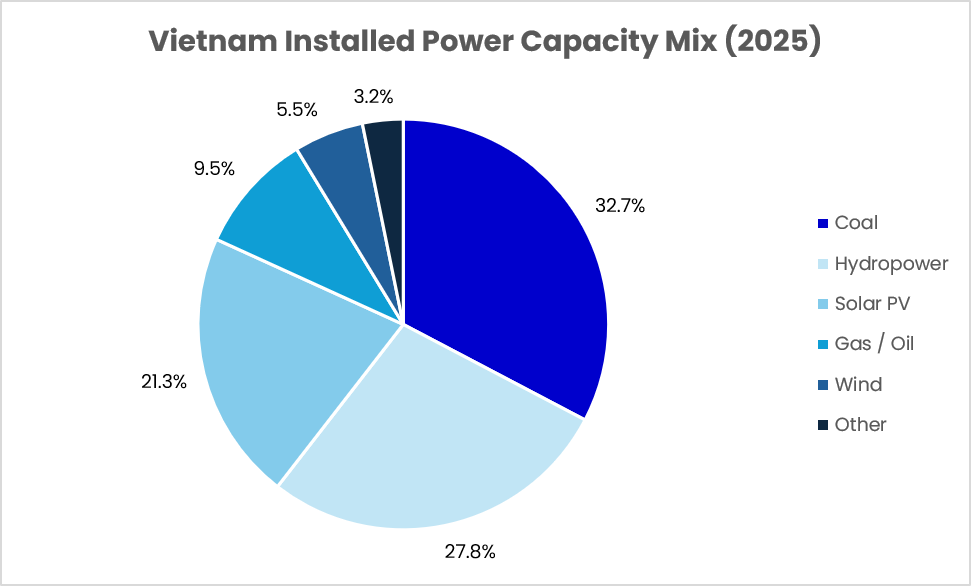

Understanding where Vietnam’s energy system currently sits is essential context for sizing the transition ahead. The 90 GW installed base at end-2025 is dominated by three roughly equal pillars: coal-fired power at approximately 32.7% of installed capacity, hydropower at 27.8%, and renewable energy — primarily solar and wind — at around 26.8%. Gas and oil-fired plants account for the remaining 9.5%, with other sources making up the balance.

Figure 2: Vietnam’s 90 GW installed capacity mix as of end-2025. Coal remains the largest single source, but solar and wind together already account for 26.8% — a share built almost entirely in the seven years since 2018. Source: Reccessary / Ministry of Industry and Trade, November 2025.

Vietnam cannot simply scale its existing system. Hydropower is near its practical ceiling, coal faces policy constraints, and gas expansion remains slow. The transition therefore depends on renewable energy, storage, and grid infrastructure growing at unprecedented scale.

How the Generation Mix Has Already Shifted

Six Years of Structural Change Visible in the Annual Output Data

Between 2019 and 2024, total electricity generation increased from approximately 198 billion kWh to 313 billion kWh. Coal generation rose from 95 billion kWh to 156 billion kWh, remaining the dominant source of electricity despite rapid renewable deployment. Hydropower output fluctuated with rainfall conditions, while solar and wind generation increased from just 1 billion kWh to approximately 49 billion kWh.

Figure 3: Vietnam’s electricity generation mix by source, 2019–2024. Coal output has grown in absolute terms but solar and wind have emerged as material contributors, rising from roughly 3% of generation in 2019 to approximately 16% by 2024. Hydropower variability reflects seasonal rainfall patterns. Source: EVN; IRENA; Ember; BloombergNEF.

The most significant structural change occurred in renewable generation. Combined solar and wind output increased from just 1 billion kWh in 2019 to approximately 49 billion kWh in 2024. Much of this growth was concentrated between 2020 and 2022, when feed-in tariff programmes triggered one of the fastest renewable deployment cycles in Southeast Asia. By 2024, solar and wind together accounted for roughly 16% of total electricity generation, compared with less than 1% five years earlier. This represents one of the most rapid shifts in Vietnam’s modern energy history and provides tangible evidence that renewable energy is moving from a supplemental resource toward a core pillar of the country’s future power system.

What the chart makes clear is that Vietnam’s energy transition has so far been largely additive rather than substitutive. Renewable generation has grown rapidly, but it has supplemented rather than displaced conventional generation. Total electricity demand has expanded quickly enough that coal generation has continued to rise in absolute terms even as renewable energy’s share of the mix has increased. This dynamic reflects the practical realities of a fast-growing emerging economy, where energy security remains as important as decarbonisation.

The 2030 Targets: Ambition in Numbers

From Feed-In Tariff to Competitive Market

The Revised PDP8 approved in April 2025 significantly increased Vietnam’s renewable energy ambitions. By 2030, solar capacity is targeted at 46–73 GW, onshore wind at 26–38 GW, offshore wind at 6 GW, and battery storage at 10–16 GW, compared with a largely negligible base today. Total installed capacity is expected to reach between 183 GW and 236 GW.

Achieving these targets will require a shift away from the feed-in tariff model that drove the solar boom. Competitive auctions and direct power purchase agreements (DPPAs) are intended to provide a more sustainable framework while reducing pressure on EVN. Under the DPPA mechanism, renewable generators can sell electricity directly to large corporate consumers, supporting market liberalisation and improving project bankability. These reforms are particularly important for offshore wind, which requires long-term financing supported by stable and creditworthy revenue structures.

The FiT Boom, the Bust, and the Implications for Future Build

Capacity Additions Reveal a Market Defined by Policy Cycles

No aspect of Vietnam’s energy transition is better illustrated by the annual data than the relationship between policy incentives and deployment pace. The chart below captures how dramatically renewable energy construction activity has responded to regulatory support, particularly during the feed-in tariff era, and how deployment patterns shifted once those incentives expired.

Figure 4: Annual solar and wind capacity additions in GW per year, 2018–2025, with cumulative solar build on the right axis. The 2019–2021 FiT-era solar rush added over 14 GW in three years; post-FiT additions collapsed sharply before recovering as the DPPA framework and Revised PDP8 emerged. Source: IRENA; EVN; Vietnam Ministry of Industry and Trade.

Solar additions peaked at approximately 10 GW in 2020 as developers rushed to meet feed-in tariff deadlines. Combined with around 4.5 GW added in 2019, Vietnam deployed more than 14 GW of solar capacity in just two years. Following the expiry of FiT incentives, solar deployment slowed sharply, while wind additions surged to nearly 4 GW in 2021 before moderating as policy support waned.

The experience highlights the importance of regulatory clarity. Vietnam has demonstrated that renewable capacity can be deployed at extraordinary speed when incentives are clear and time-bound. The next phase of growth will depend less on fixed tariffs and more on the successful implementation of competitive auctions, DPPAs, and other market-based mechanisms capable of supporting long-term investment.

Offshore Wind: Vietnam’s Highest-Stakes Investment Frontier

The Resource Is Proven; the Regulatory Framework Is Still Forming

Vietnam possesses one of the highest offshore wind resource endowments in Southeast Asia. Its 3,200 km of coastline includes shallow-water zones well-suited for fixed-bottom turbine foundations, with wind speeds in key areas that compare favourably with established European offshore markets. The World Bank’s July 2025 report on Vietnam’s offshore wind sector identified the country’s resource quality as a genuine competitive advantage — one that explains the interest of major global developers despite the relatively nascent regulatory environment.

The long-term potential is substantial. The Revised PDP8 targets between 113 GW and 139 GW of offshore wind capacity by 2050, positioning Vietnam among the world’s largest potential offshore wind markets. However, the near-term challenge is execution. As of mid-2026, no commercial-scale offshore wind project has received formal investment approval, placing the 6 GW target for 2030 at significant risk.

The regulatory framework is evolving rapidly. National Assembly Resolution 253/2025 streamlines approvals by allowing investment policy and investor selection to proceed simultaneously, while Decree 58/2025 introduced minimum capital requirements for developers. The February 2026 award of the 750 MW Hon Trau project to VinEnergo marked the first formal allocation of a commercial-scale offshore wind project and signalled the government’s intention to accelerate sector development.

Where the Institutional Opportunity Sits

A USD 136 Billion Investment Programme Across the Energy Stack

Meeting Vietnam’s 2026–2030 power development targets will require approximately USD 136 billion of investment, including USD 118 billion for generation and USD 18 billion for transmission infrastructure. The scale of funding required makes private and foreign capital participation essential, particularly as recent regulatory reforms now permit non-state ownership of transmission and substation assets.

For institutional investors, opportunities extend beyond generation projects themselves. Offshore wind development will require experienced equity partners, international project finance, and collaboration between domestic developers and global technology providers. The broader offshore wind ecosystem—including component manufacturing, port infrastructure, battery storage, grid modernisation, and operations and maintenance services—offers multiple avenues for capital deployment across the energy value chain.

Risks and Structural Headwinds

Policy Credibility, Grid Constraints, and Bankability

Vietnam’s energy transition faces three key risks that institutional investors must monitor closely. The first is regulatory credibility. Retroactive tariff reductions for existing solar and wind projects have raised concerns about long-term revenue certainty, an important consideration for capital-intensive assets such as offshore wind. The second is grid integration. Vietnam’s rapid renewable buildout has previously outpaced transmission development, creating curtailment risks and highlighting the importance of timely grid expansion. The third is offtake structure. While direct power purchase agreements (DPPAs) reduce reliance on EVN as a sole buyer, the mechanism remains relatively new and must demonstrate sufficient scale, stability, and lender acceptance to support the next generation of large-scale renewable projects.

Closing the Gap: Vietnam’s Power Transition as an Institutional Theme

Vietnam’s energy transition is a structural investment theme driven by strong electricity demand growth, industrial expansion, and the need to diversify a coal-heavy power system. The USD 136 billion investment programme under the Revised PDP8 highlights both the scale of the opportunity and the growing role of private capital in financing Vietnam’s energy future.

For institutional investors, the most attractive opportunities extend beyond generation assets themselves. Battery storage, transmission infrastructure, DPPA-based energy procurement, offshore wind supply chains, and grid modernisation all stand to benefit from the next phase of renewable deployment. While offshore wind offers significant long-term potential, the broader ecosystem surrounding Vietnam’s energy transition may provide the most immediate and scalable avenues for investment.

Vietnam’s energy transition is ultimately a story of scale. Meeting demand growth, modernising the power system, and achieving renewable targets will require more than USD 136 billion of investment within the next five years alone. Whether offshore wind reaches its targets or not, the direction of travel is clear: capital will need to flow into generation, transmission, storage, and grid modernisation at unprecedented levels. For investors, the question is no longer whether Vietnam’s energy system will expand, but where along the value chain the most attractive opportunities will emerge.

For deeper insights on capital markets, infrastructure investment, and emerging market opportunities across Southeast Asia, follow DealFlow for research-driven perspectives via LinkedIn or explore further analysis at DealFlow.sg.