Vietnam’s investment story is usually framed through manufacturing relocation, foreign direct investment, and the rise of its export economy. Yet the next phase of the country’s competitiveness may be decided by something less visible but equally decisive: the infrastructure layer that moves goods from factory floor to port, warehouse, retailer, consumer, and export market. Logistics is no longer a back-office operating cost for Vietnam. It is becoming a strategic asset class at the intersection of trade, digital commerce, food security, industrial real estate, and private capital.

The structural logic is straightforward. Vietnam has already proven that it can absorb global manufacturing flows. The harder question is whether it can build the logistics depth required to support higher-value production, shorter delivery cycles, temperature-controlled supply chains, and more resilient domestic distribution. As export volumes rise and consumer channels fragment, legacy logistics models built around basic transport and low-cost warehousing are becoming insufficient. The investable opportunity is therefore shifting from generic trucking capacity toward integrated logistics platforms, cold storage, fulfilment networks, bonded warehouses, port connectivity, inland waterways, and technology-enabled supply chain services.

The Repricing of Vietnam’s Supply Chain Backbone

Export Scale Has Outgrown Legacy Logistics

Figure 1: Vietnam’s trade engine continues to expand at institutional scale, with merchandise exports rising from roughly USD 353.1 billion in 2023 to USD 405.5 billion in 2024, while imports also climbed sharply.

Vietnam’s supply chain base has moved beyond treating logistics as a low-value support service. According to World Bank WITS data, Vietnam recorded USD 353.1 billion of merchandise exports and USD 325.4 billion of merchandise imports in 2023, against GDP of about USD 433.9 billion. Reuters reported that by 2024, exports had risen 14.3% to USD 405.53 billion, imports increased 16.7% to USD 380.8 billion, and GDP reached USD 476.3 billion. Vietnam is effectively operating an economy where trade flows are nearly the size of domestic output, making logistics performance central to macro competitiveness.

This matters because the country’s export model is becoming more demanding. Electronics, apparel, furniture, food products, agricultural goods, and seafood each have distinct logistics needs. Electronics require predictable component movement and export documentation. Apparel and footwear depend on shorter lead times. Seafood, frozen foods, and fresh produce require reliable cold chain handling. As multinational manufacturers embed Vietnam into regional production networks, the margin for logistics failure narrows. Delayed customs clearance, limited storage, weak inland connectivity, or poor temperature control can directly affect customer retention, inventory costs, and working capital efficiency.

The old logistics model was volume-driven: move containers, store inventory, and compete on price. The new model is service-driven: visibility, reliability, compliance, cold chain integrity, and multi-node distribution. That shift creates room for professional operators with stronger systems, broader customer relationships, and the capital to invest ahead of demand.

Logistics Costs Are Becoming a National Competitiveness Issue

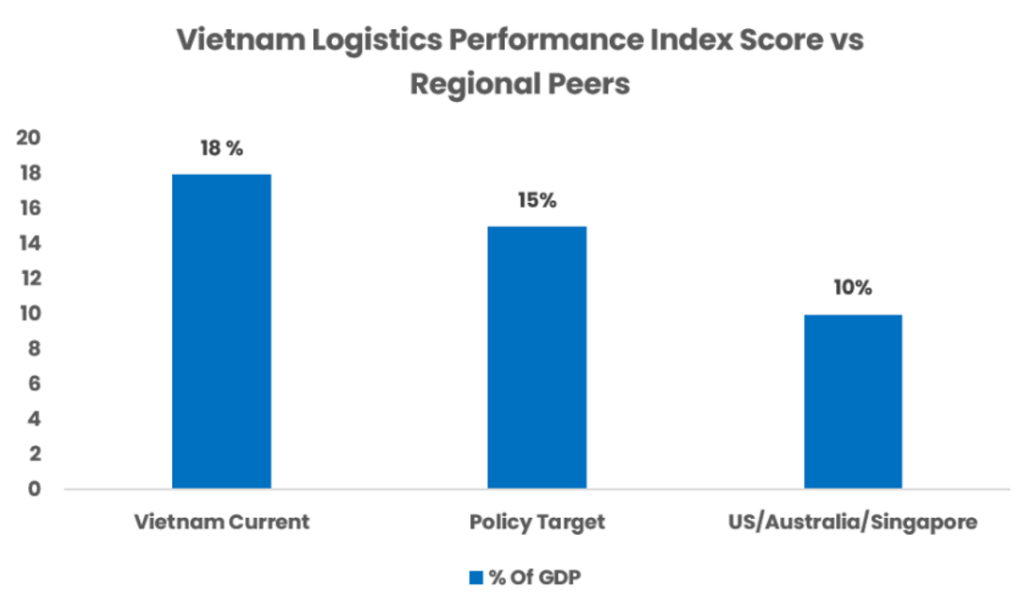

Figure 2: Vietnam is explicitly trying to reduce logistics costs from high-teen levels toward 15% of GDP, while World Bank analysis notes that costs remain materially above advanced-market benchmarks.

Vietnam’s high logistics costs show that the sector has not yet caught up with the country’s trade ambitions. At the Vietnam Logistics Forum 2024, the Prime Minister said Vietnam needed to reduce logistics costs from around 18% of GDP to 15%. A World Bank document separately estimated logistics costs at about 20% of GDP, far above markets such as the United States, Australia, and Singapore, where costs are below 10%.

This is not just a cost issue. It directly affects export competitiveness. As labor costs rise and tariff advantages narrow, Vietnam’s next productivity gains must come from better logistics: fewer delays, stronger port access, improved warehousing, lower spoilage, smoother customs, and more efficient transport networks.

For investors, the policy signal matters. If logistics cost reduction is a national priority, then ports, inland waterways, logistics centers, customs digitalization, and industrial infrastructure are likely to receive stronger policy support. Execution risk remains, but the sector is clearly aligned with Vietnam’s long-term development agenda.

The Demand Shock: E-Commerce, Cold Chain and Higher Service Standards

Digital Consumption Is Pulling Warehousing Closer to the Consumer

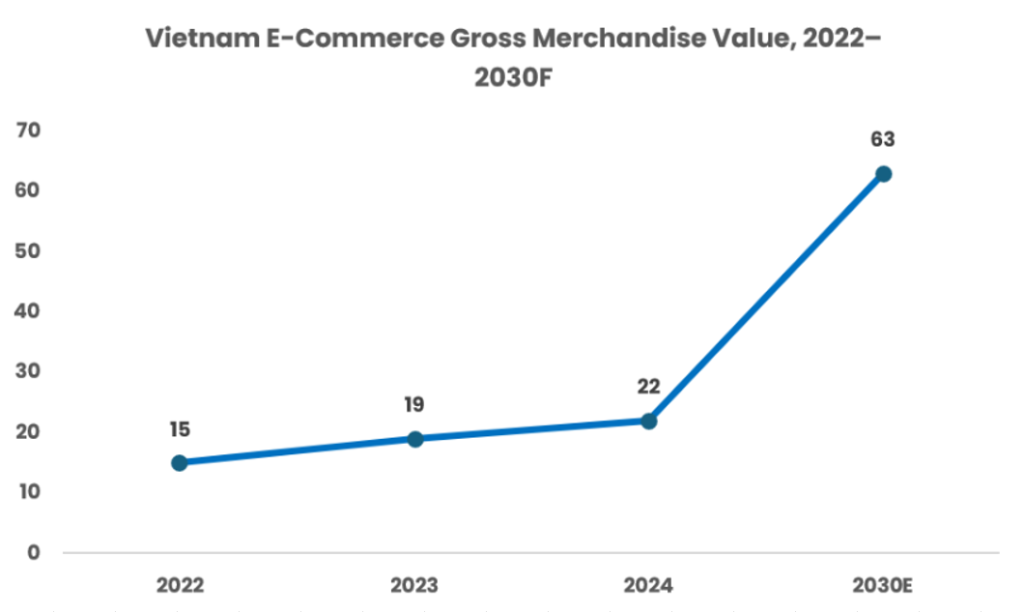

Figure 3: Vietnam’s e-commerce GMV increased from USD 15 billion in 2022 to USD 22 billion in 2024 and is projected by Google, Temasek, and Bain analysis to reach roughly USD 63 billion by 2030.

The second driver of logistics repricing is domestic digital consumption. The Google, Temasek, and Bain e-Conomy SEA 2024 Vietnam report estimates that Vietnam’s e-commerce GMV expanded from USD 15 billion in 2022 to USD 19 billion in 2023 and USD 22 billion in 2024, with a pathway toward roughly USD 63 billion by 2030. This shifts the logistics problem from long-haul export movement to dense, fragmented, high-frequency fulfilment.

E-commerce changes what good logistics looks like. Instead of moving bulk goods between factories, ports, and distributors, operators must manage SKU-level inventory, reverse logistics, urban last-mile delivery, parcel sorting, multiple payment methods, and promotional spikes. The focus moves from transport alone toward fulfilment capability: warehouse automation, route optimization, customer data integration, inventory accuracy, and absorbing demand peaks without service breakdowns.

This creates a natural opening for platform consolidation. Fragmented logistics providers can compete in simple delivery, but often struggle to provide nationwide visibility, standardized service levels, and integrated warehouse-to-door solutions. As consumer brands, marketplaces, and retailers professionalize, they need logistics partners that can scale with them. Institutional capital can fund multi-city warehouse networks, automation capex, technology systems, and consolidation strategies that turn local operators into credible platforms.

Cold Chain Is Becoming a Premium Infrastructure Vertical

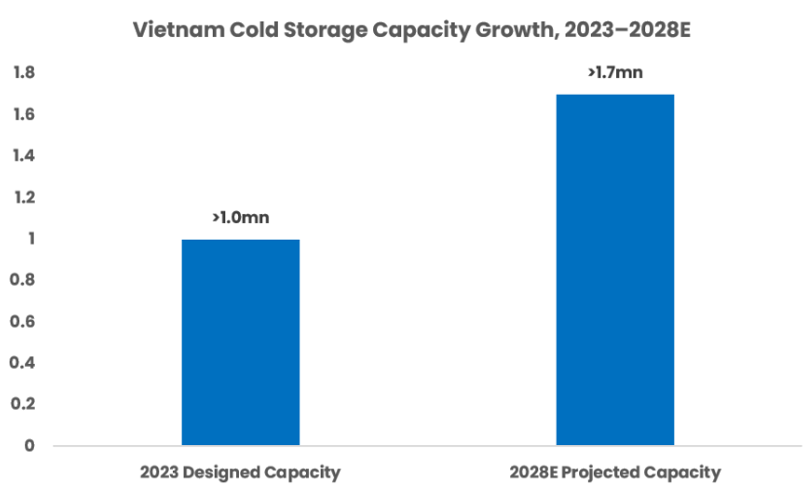

Figure 4: Vietnam’s commercial cold storage capacity exceeded 1.0 million pallets in 2023 and is projected by FiinGroup to reach more than 1.7 million pallets by 2028.

Cold chain is the clearest example of Vietnam’s logistics infrastructure gap becoming investable. FiinGroup reported that Vietnam’s cold chain logistics market reached USD 211.2 million in 2023, with 101 commercial cold storage providers and designed capacity of over 1.0 million pallets. Capacity is projected to exceed 1.7 million pallets by 2028, supported by 13 new projects during 2024–2028.

Demand is broad-based. Seafood exports need temperature control from processing to port, while fresh produce, meat, pharmaceuticals, vaccines, online grocery, and fresh-food delivery all require reliable cold-chain handling. In these markets, supply chain failure can directly destroy product value through spoilage, temperature excursions, failed deliveries, or inconsistent handling.

For investors, cold chain is attractive because it combines real estate, infrastructure, and operational specialization. Assets are capex-heavy and location-sensitive, while customers often pay a premium for reliability. However, cold chain is more complex than ordinary warehousing. Electricity costs, utilization volatility, maintenance needs, food safety standards, and customer concentration can pressure margins without clear contracted demand.

Where the Institutional Opportunity Sits

From Transport Operators to Integrated Logistics Platforms

The core investment opportunity is not simply buying more trucks or building more warehouses. Vietnam already has many fragmented providers across freight forwarding, trucking, storage, customs brokerage, and last-mile delivery. The stronger opportunity is to institutionalize the sector by building integrated platforms that solve several pain points for the same customer.

Manufacturers need more than transport; they need inbound components, inventory staging, export documentation, customs handling, port movement, packaging, and shipment visibility. Retailers need more than warehouse space; they need SKU management, store replenishment, online fulfilment, return handling, and reliable delivery. Seafood exporters need more than cold rooms; they need temperature control, refrigerated trucking, port access, documentation, and customer assurance. Value will shift toward operators that can bundle these services into one accountable relationship.

This makes logistics platform-building a natural private equity and strategic investor theme. Fragmented markets create room for consolidation, operating improvements can lift margins, technology can improve customer retention, and regional expansion can diversify demand. Once a platform reaches sufficient scale, it can command higher valuation multiples than single-site or single-service operators.

Capital Stack Fit: Real Estate, Private Equity and Private Credit

Logistics infrastructure fits several capital strategies. Real estate investors can finance warehouses, logistics parks, cold storage, and fulfilment centers backed by long-term leases. Private equity investors can build integrated platforms by acquiring fragmented providers and funding expansion. Private credit providers can support capex-heavy projects with contracted cash flows that need more flexible financing than banks typically provide.

The strongest assets will combine these strategies. Cold storage, fulfilment, and port-adjacent logistics platforms often require facility capital, equipment financing, operating expertise, and working capital. As these assets become more institutional, they can support more sophisticated structures such as sale-and-leasebacks, asset-backed financing, infrastructure debt, strategic joint ventures, and eventually REIT-like vehicles.

Risks and Structural Headwinds

Fragmentation, Margins and Execution Risk

The opportunity is real, but it is not risk-free. The first challenge is fragmentation. Vietnam’s logistics sector includes thousands of small operators with limited technology, uneven service quality, and thin balance sheets. Fragmentation creates acquisition opportunities, but it also makes integration difficult. Systems may not communicate with one another. Customer contracts may be informal. Management teams may be founder-led. Pricing discipline may be weak. Consolidation only creates value if operational execution improves after the transaction.

The second challenge is margins. Logistics can look attractive at the revenue level but disappointing at the profit level if operators compete mainly on price. Fuel costs, labor costs, electricity prices, equipment maintenance, land rents, and underutilized capacity can quickly erode returns. Cold chain is particularly exposed because facilities require high energy intensity and must maintain reliable temperature control even when utilization fluctuates.

The third challenge is customer concentration. Many logistics providers grow around a small number of anchor customers. This can support early expansion, but it can also create bargaining power issues and revenue volatility if the customer changes sourcing strategy, shifts warehouse footprint, or brings logistics in-house. Institutional investors should therefore focus not only on revenue growth but also on contract quality, customer diversification, retention rates, and service-level performance.

Land, Energy and Regulatory Constraints

The second category of risk relates to physical and regulatory constraints. Logistics assets are highly location-dependent. Warehouses near ports, ring roads, industrial parks, airports, and dense urban catchments are more valuable because they reduce transit time and improve utilization. But land access in these areas is competitive, permitting can be slow, and infrastructure bottlenecks can undermine otherwise sound projects.

Energy reliability and cost are especially important for cold storage and automated fulfilment. A refrigerated facility is not simply a warehouse with cooling equipment; it is an energy-dependent infrastructure asset. Investors need to underwrite electricity tariffs, backup systems, insulation quality, equipment efficiency, and maintenance capability. Poor engineering or weak operations can turn a promising cold chain project into a margin trap.

Regulatory and compliance standards will also become more important as Vietnam moves into higher-value logistics. Food safety, pharmaceutical distribution, customs compliance, bonded warehousing, environmental standards, and data visibility all raise the operating bar. This favors professional operators but increases the cost of institutionalization.

Closing the Gap: Vietnam’s Next Infrastructure Investment Theme

Vietnam has built one of Southeast Asia’s strongest export platforms. The next challenge is building the logistics system to support its next phase of growth. With exports above USD 400 billion, high logistics costs, e-commerce GMV projected to reach around USD 63 billion by 2030, and cold storage capacity set to expand through 2028, logistics is becoming a critical growth bottleneck.

For institutional capital, the opportunity is structural rather than speculative. Demand is already visible across manufacturing, retail, agriculture, seafood, pharmaceuticals, and digital commerce. The best opportunities will come from platforms with strategic locations, reliable service, and the ability to solve complex customer needs.

Vietnam’s logistics opportunity is ultimately a repricing of its supply chain backbone. As trade, consumption, and cold chain demand grow, investors that combine infrastructure capital with operational discipline will be best positioned to capture the next stage of market development.

For deeper insights on capital markets, infrastructure investment, and emerging market opportunities, follow DealFlow for research-driven perspectives on global finance via LinkedIn or explore further analysis at DealFlow.sg.