Vietnam’s growth story has often been told through factories, exports, consumer spending, and foreign direct investment. Yet the next stage of urban productivity may be decided by a more basic question: how efficiently people can move through the country’s largest cities. Hanoi and Ho Chi Minh City are no longer only expanding outward; they are becoming denser, more complex metropolitan economies where congestion, air quality, commuting time, and land-use efficiency directly affect competitiveness.

Urban mobility is therefore shifting from a public-works discussion into an institutional infrastructure theme. For decades, Vietnam’s cities adapted around the motorbike: flexible, low-cost, and suited to narrow streets. That model helped cities grow quickly, but it is becoming harder to scale. Higher household incomes, rising car ownership, delivery traffic, ride-hailing, and e-commerce deliveries are making road-based mobility less efficient. The investment opportunity is not simply more roads. It is the creation of a rail-led, digitally integrated, higher-capacity mobility system that can support urban growth without turning congestion into a structural tax on the economy.

The Urbanization Pressure Behind Vietnam’s Mobility Reset

Urban Growth Is Forcing a Higher-Capacity Transport Model

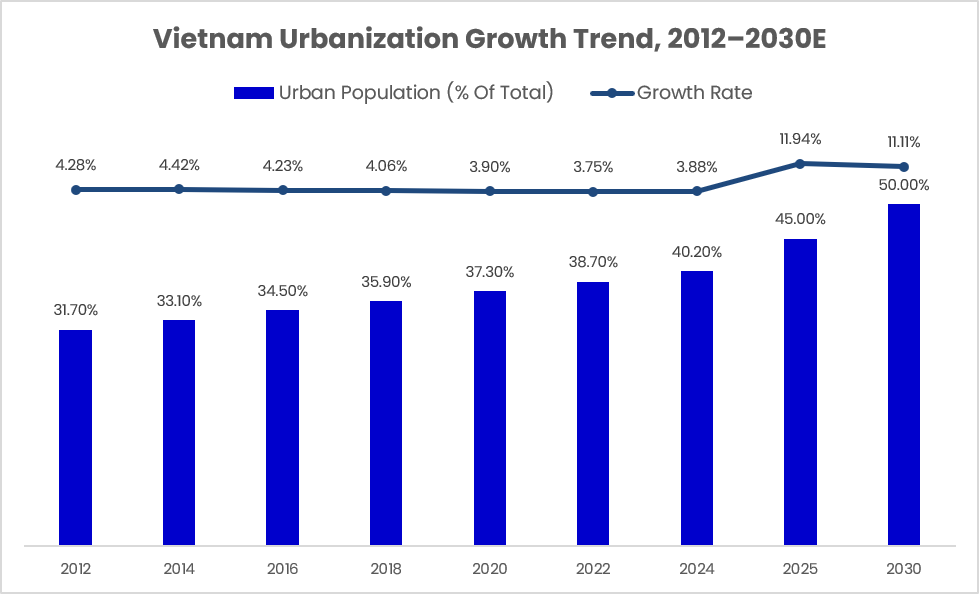

Vietnam is still less urbanized than many regional peers, but the direction is clear and increasingly difficult to ignore. World Bank data based on UN World Urbanization Prospects show the urban population share rising steadily over the past decade, with Vietnam moving from around 30.4% urbanization in 2010 to above 40% by 2024. The chart highlights the upward trend from 2012 onward, while the growth-rate line shows that urbanization has continued to expand consistently across each measured period.

The policy direction points to a further step-change. Vietnam’s national urbanization rate is targeted at around 45% by 2025 and approximately 50% by 2030. This matters because transport systems are path-dependent: cities that wait until density is already locked in often face higher land-acquisition costs, more disruptive construction, and lower flexibility in route planning. Urban rail, therefore, is not only a response to current congestion; it is a forward-looking investment in how Vietnam’s cities will function as they become more urbanized.

The immediate pressure is visible in Hanoi and Ho Chi Minh City. Private two-wheelers remain the default mobility tool, but they are less effective when combined with rising car ownership, logistics traffic, ride-hailing, and online delivery flows. The policy question is therefore not whether Vietnam needs mass transit, but how quickly it can create a system reliable enough to change commuter behaviour. Public transport must become attractive before restrictions on private vehicles become socially and economically workable.

The timing matters because urbanization is not only a population statistic. It changes the economic geography of demand. More people living and working in metropolitan areas means more peak-hour commuting, more school and healthcare trips, more delivery traffic, and stronger pressure on roads that were not designed to absorb unlimited private-vehicle growth. Without higher-capacity public transport, urban expansion can dilute productivity gains: households spend more time commuting, firms face a smaller effective labour pool, and central districts become harder to access. Metro investment is therefore best understood as economic capacity infrastructure, not simply a transport amenity.

Figure 1: Vietnam’s urbanization has moved steadily upward since 2010, while 2025 and 2030 policy targets imply a faster transition toward majority-urban status.

Source: World Bank (Urban Population % of Total Population, based on UN World Urbanization Prospects); Government of Vietnam (2025 & 2030 urbanization targets).

Metro Networks Are Moving From Symbolic Projects to System Buildout

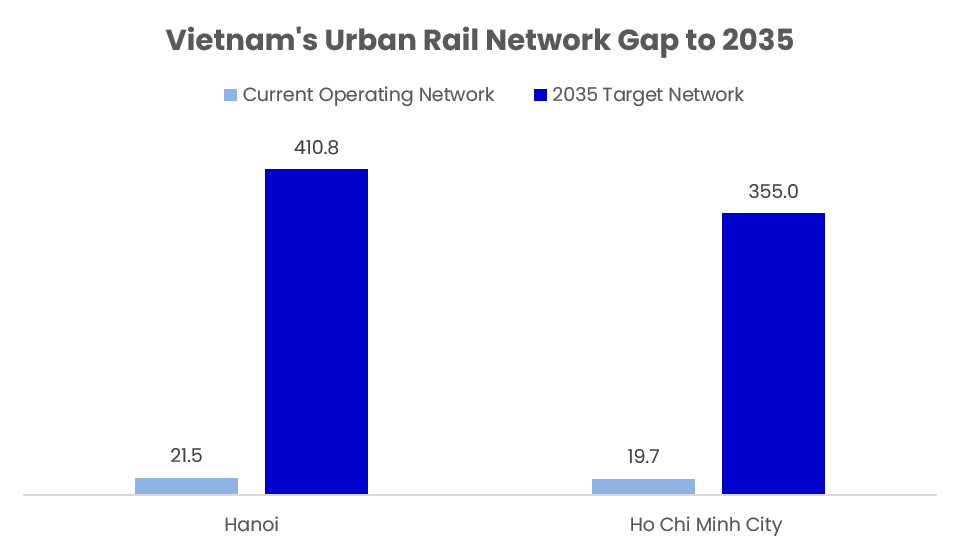

The First Lines Prove Operation, but the Network Gap Remains Large

Vietnam has moved beyond the question of whether urban rail can operate. Hanoi’s Cat Linh–Ha Dong line is already in service, the elevated section of the Nhon–Hanoi Station line has begun operations, and Ho Chi Minh City’s Metro Line 1 started commercial service in late 2024. These early lines are important because they prove that metro systems can be delivered and operated in Vietnam’s two largest cities.

The more important point is that these first lines are only the operating base, not the target system. Hanoi currently has around 21.5 km of operating urban rail, compared with a 2035 target network of roughly 410.8 km. Ho Chi Minh City’s operating network is essentially Metro Line 1 at about 19.7 km, against a 2035 target of around 355 km. The chart makes the gap clear: both cities are at the beginning of a much larger network buildout.

This is the core investment logic. Vietnam’s metro market is moving from isolated flagship projects toward a decade-long system expansion. Once multiple lines operate as a network, stations can become commercial nodes, ticketing can become integrated, feeder routes can be planned around rail capacity, and land-use policy can concentrate density around transit corridors rather than spreading growth along already-congested roads.

Figure 2: Hanoi and Ho Chi Minh City have proven that urban rail can operate, but their 2035 targets remain many times larger than the current base. Source: Hanoi People’s Committee; Ho Chi Minh City People’s Committee (Urban Railway Master Plans, 2035 targets).

Ridership Is the First Test of Behavioral Change

Hanoi’s Metro Usage Shows Early Adoption Momentum

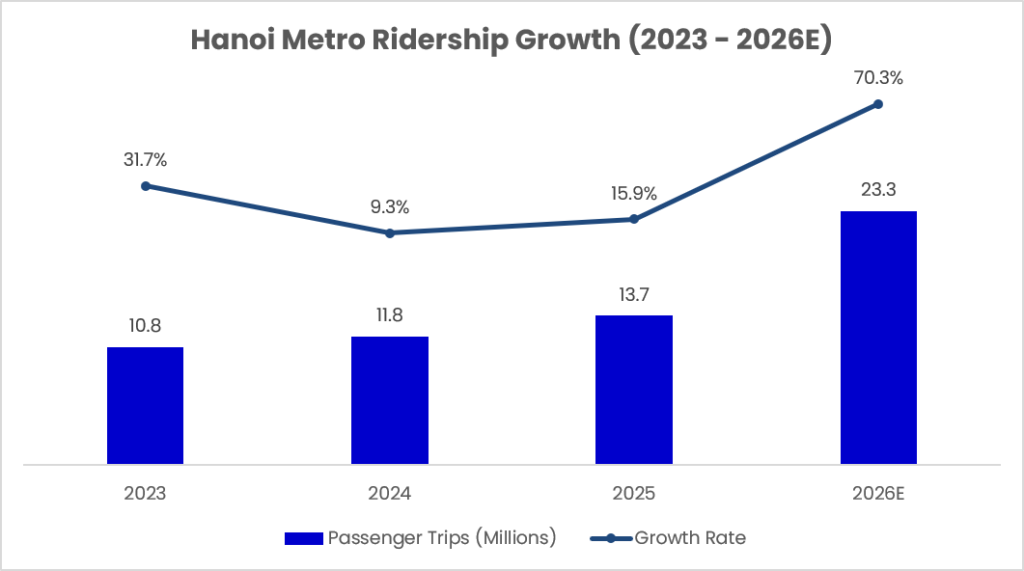

The strongest evidence that urban rail can become more than symbolic infrastructure is actual passenger usage. Hanoi’s metro ridership has been rising, with passenger trips increasing from around 8.2 million in 2022 to 10.8 million in 2023, 11.8 million in 2024, and approximately 13.68 million in 2025. This is still early-stage adoption, but the direction is positive.

The significance is not only that ridership is growing. It is that the system is beginning to create a behavioural proof point. Urban rail depends on habit formation: commuters must trust that trains are reliable, affordable, accessible, and sufficiently connected to daily destinations. Once ridership grows, the case for feeder buses, integrated ticketing, station retail, last-mile connections, and transit-oriented development becomes stronger.

Hanoi’s ridership growth also shows why network expansion matters. A single line can attract users along one corridor, but ridership potential increases materially when lines connect with one another and serve more employment, residential, education, and commercial nodes. The metro becomes more useful as the network becomes denser. This is why the gap between current operations and 2035 targets is not merely a construction target; it is a demand-creation pathway.

Figure 3: Hanoi metro ridership has increased steadily since 2022, showing early evidence that urban rail can gain commuter adoption as service reliability and network coverage improve. Source: Hanoi Metro Company (2023–2025 ridership data)

Where the Institutional Opportunity Sits

From Construction Packages to Mobility Platforms

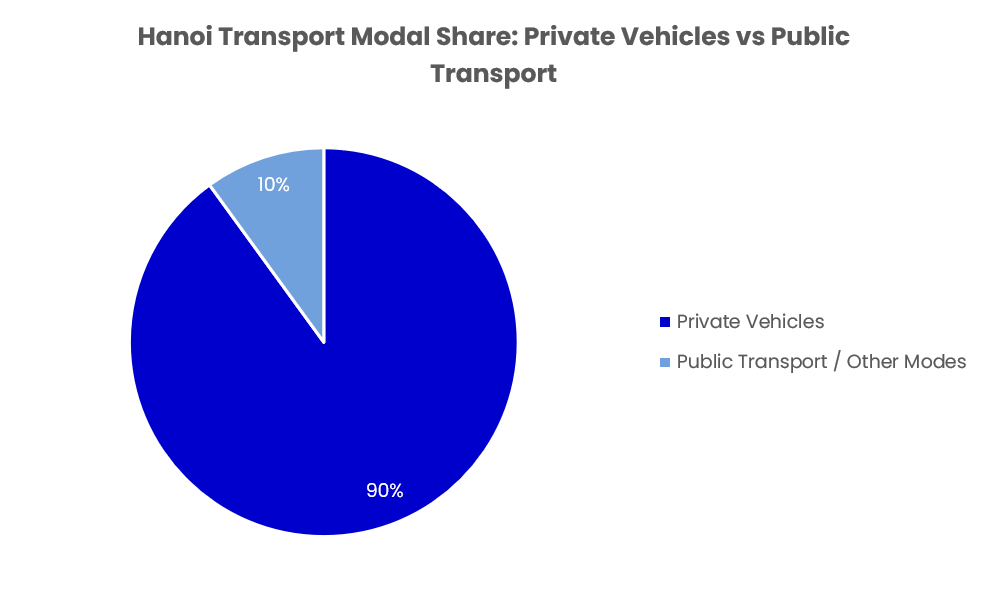

The most investable mobility theme is unlikely to be a pure concession on farebox revenue alone. The baseline modal mix explains why: private vehicles account for about 90% of Hanoi’s transport modal share, leaving only a small share for public transport and other modes. This means rail is not replacing a mature public transit system; it is creating the backbone that allows public transport to compete with private mobility. This private-vehicle dependence is exactly why urban rail is strategically important. A city where private vehicles dominate mobility can continue expanding roads, but that approach becomes less efficient as density rises. More roads often invite more vehicles, while road space in central districts remains limited. Rail offers a different model: higher capacity, more predictable journey times, lower land intensity per passenger, and the ability to support denser development around stations.

For investors, the stronger opportunity lies in the ecosystem around mobility: engineering and construction packages, signaling and control systems, rolling stock, depot equipment, station operations, ticketing and payments, transit-oriented development, advertising, retail concessions, parking systems, feeder bus networks, and data-driven mobility services. The rail line is the anchor, but the commercial opportunity extends across the full urban transport stack.

This creates several capital-stack entry points. Public budgets and government bonds can finance core infrastructure. Official development assistance and concessional loans can support large packages and project preparation. Strategic investors and contractors can participate through EPC, operations and maintenance, and equipment supply. Real estate investors can underwrite station-area development where planning rules allow value capture. Private credit can support equipment, depots, rolling-stock-adjacent facilities, and contracted service providers.

Figure 4: Hanoi’s baseline mobility mix shows why metro investment is a structural policy priority. Source: C40 Cities reports private vehicles account for about 90% of transport modal share, leaving only a small share for public transport and other modes.

Risks and Structural Headwinds

Execution, Funding and Ridership Will Decide the Pace

The opportunity is large, but Vietnam’s rail transition carries material execution risk. The first risk is delivery. The early metro projects in both major cities show how land clearance, design changes, procurement complexity, funding delays, and contractor coordination can stretch timelines. Scaling from a few operating lines to hundreds of kilometres will require stronger project governance, standardized technical rules, and faster approval processes. The second risk is funding. The two-city urban rail programme is institutional in scale and cannot be solved by fare revenue alone. It requires a layered model that combines central and municipal budgets, government bonds, official development assistance, concessional loans, land-value capture, and selective private-sector participation. A rail line is not just a construction asset; it is a multi-decade operating obligation. Investors need to underwrite lifecycle costs, maintenance discipline, electricity costs, staffing, safety systems, and fare-policy assumptions.

This is why funding structure will matter as much as headline capex. Urban rail rarely becomes financially sustainable through ticket revenue alone in the early years; it usually needs a wider value-capture framework that links rail investment to land values, commercial space, station retail, advertising, and adjacent real estate development. Vietnam’s challenge will be to convert those wider economic benefits into bankable cash flows without overburdening households or relying entirely on public budgets.

The third risk is ridership integration. Metro lines create value only if they connect well with where people live, work, study, and shop. Poor feeder buses, inconvenient walking access, weak park-and-ride design, or fragmented ticketing can limit adoption. The social challenge is equally important: Vietnam cannot simply restrict motorbikes without providing reliable, affordable alternatives. Policy must sequence supply before restriction.

The fourth risk is value capture. Metro lines can raise land values, but unless cities have the tools to capture part of that uplift through land auctions, development rights, taxes, station concessions, or joint development, the public sector bears the capex while private landholders capture much of the upside. For the mobility reset to be financially sustainable, Vietnam will need to connect rail planning with land-use planning, commercial development, and long-term operating discipline.

Closing the Gap: Vietnam’s Next Urban Infrastructure Theme

Vietnam’s urban mobility reset is still early, but the direction is now visible. Urbanization is rising, the first metro systems are operating, Hanoi and Ho Chi Minh City have set large network targets, and policy is moving toward special mechanisms to accelerate urban rail development. Together, these signals point to a new infrastructure cycle built around mobility capacity rather than road expansion alone.

For institutional capital, the opportunity is structural rather than speculative. The strongest themes will be those that sit between public necessity and commercial scalability: station-area development, systems integration, O&M platforms, ticketing and payments, rolling-stock supply chains, feeder networks and mobility-linked real estate. The winners will not be investors chasing isolated projects, but those able to understand the full urban transport stack.

Vietnam built its early urban economy on the flexibility of the motorbike. Its next urban phase will require the reliability of networks. As metro and transit-oriented infrastructure move from planning documents into execution, mobility is becoming one of Vietnam’s most important institutional infrastructure frontiers.

For deeper insights on capital markets, infrastructure investment, healthcare platforms, and emerging market opportunities, follow DealFlow for research-driven perspectives on global finance via LinkedIn or explore further analysis at DealFlow.sg.