Vietnam’s next investable consumer theme may not be another retail channel, delivery platform, or digital wallet. It may be the infrastructure of care itself. For years, healthcare in Vietnam has been viewed mainly as a public-service obligation: crowded hospitals, insurance coverage, medicine access, and government budget pressure. That framing is no longer enough. A larger middle class, an older population, higher chronic-disease burden, and rising willingness to pay are turning healthcare into a long-duration private capital theme.

The opportunity is broader than hospital construction. The deeper shift is toward organised care platforms: specialty clinics, diagnostics, outpatient chains, rehabilitation, dental, eldercare, preventive screening, and insurance-linked services. Private healthcare can grow by solving visible household pain points: waiting time, service quality, specialist access, and continuity of care.

For investors, the question is where demand converts into recurring revenue, defensible brand equity, and scalable operating models rather than isolated medical assets. Vietnam’s care economy is beginning to answer that question.

The Demand Reset Behind Vietnam’s Healthcare Market

Ageing Is Moving Healthcare From Episodic Need to Recurring Consumption

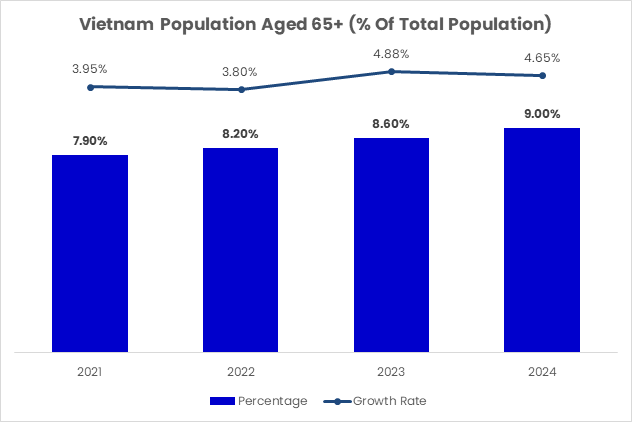

Figure 1: Vietnam’s population aged 65 and above rose from about 7.6% in 2020 to roughly 9.0% in 2024, showing how care demand is shifting toward chronic, preventive, and long-term services. Source: World Bank / FRED.

Ageing changes the economics of healthcare because it changes frequency. A young population uses healthcare mainly for acute episodes. An older population uses healthcare more continuously through diagnostics, medication management, cardiology, oncology, diabetes care, ophthalmology, rehabilitation, and follow-up consultations. That pushes the market away from one-off treatment and toward lifetime patient relationships.

Vietnam is still younger than Japan, South Korea, or Thailand, but the direction is clear. World Bank data show the 65+ population share rising every year from 2020 to 2024. Healthcare infrastructure takes time to build, so operators that wait until demographic pressure is obvious may face higher land costs, tighter talent supply, and stronger incumbent brands.

The most attractive implication is the growth of care journeys. A diabetes patient may need blood tests, medication, nutrition advice, and specialist referrals. An elderly patient may need physiotherapy, home nursing, and monitoring. These are repeated interactions, not single transactions.

Health Spending Is Rising, but the Market Still Has Room to Institutionalize

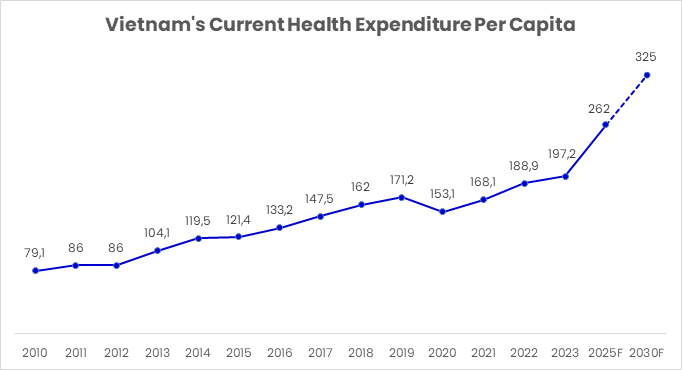

Figure 2: Vietnam’s current health expenditure per capita rose from around USD 79 in 2010 to about USD 197 in 2023, before forecast estimates suggest it could reach roughly USD 262 by 2025 and USD 325 by 2030. Source: World Bank, WHO GHED, industry estimates.

Vietnam’s healthcare spending base remains modest by regional and developed-market standards, but the long-term direction is clearly investable. Current health expenditure per capita increased from about USD 79 in 2010 to around USD 197 in 2023, reflecting more than a decade of rising formal healthcare consumption. After a temporary decline in 2020, likely linked to pandemic-related disruption and changes in healthcare utilization, spending recovered to USD 168 in 2021, USD 189 in 2022, and about USD 197 in 2023. Forecast estimates suggest the figure could rise further to roughly USD 262 by 2025 and approximately USD 325 by 2030.

This creates a middle-income healthcare setup. Spending is high enough for households to pay for better service when the value proposition is clear, but still low enough that formal healthcare consumption has years of growth ahead. As incomes rise, households tend to shift from delayed treatment to earlier diagnosis, from basic facilities to branded clinics, and from reactive care toward preventive health, diagnostics, dental, maternity, wellness, and chronic disease management.

The private market is also supported by friction in the public system. Public hospitals remain essential, but many patients associate them with long queues, administrative complexity, overcrowding, and inconsistent patient experience. Private operators can compete on convenience: appointment booking, shorter waiting times, modern equipment, integrated payments, cleaner facilities, and clearer doctor-patient communication.

Healthcare should therefore be analysed less like a cyclical consumer sector and more like essential services infrastructure. Demand is need-based, demographic support is long-term, and spending can increase as quality improves. However, medical trust, doctor recruitment, regulatory compliance, insurance relationships, and clinical governance matter more than pure expansion speed.

Where Private Capital Can Actually Build Platforms

The Hospital Gap Is Real, but Ownership Mix Matters

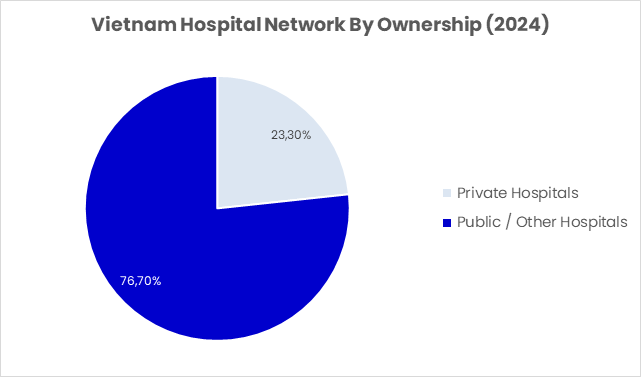

Figure 3: Vietnam had about 1,645 hospitals in 2024, including 384 private facilities. Private hospitals accounted for roughly 23% of the hospital network by facility count, but the broader private sector remains more concentrated in urban, higher-income catchments. Source: VietnamPlus, citing Vietnam healthcare sector review.

Vietnam’s private hospital presence is no longer marginal. VietnamPlus reported that the country had 1,645 hospitals in 2024, including 384 private facilities. Private participation has become structurally relevant, but capacity remains uneven. Private hospitals are more likely to cluster in major cities and affluent provinces, while public facilities carry much of the national burden.

For investors, this distinction matters. Buying or building a hospital is not automatically a platform strategy. A hospital is capital intensive, doctor dependent, regulation heavy, and vulnerable to utilization volatility if it lacks brand strength or referral depth. The better opportunity may sit in asset-light or mid-capex models that feed the hospital ecosystem: diagnostics, outpatient specialty clinics, ambulatory surgery, maternity services, dental chains, dialysis, eye care, rehabilitation, preventive screening, and medical imaging.

These formats can scale more modularly than large hospitals. A diagnostic network can standardize procurement, lab processes, reporting, and referrals. A specialty clinic chain can replicate operating protocols and patient acquisition. A rehabilitation or eldercare platform can expand through catchment-level facilities. Value comes from repeatable systems rather than a single flagship asset.

The platform thesis also fits Vietnam’s fragmented provider base. Many clinics are founder-led, locally trusted, and operationally small. That creates room for consolidation if the consolidator improves quality control, compliance, procurement, digital systems, and doctor retention.

Patient Volumes Show Why Convenience Is Becoming a Competitive Advantage

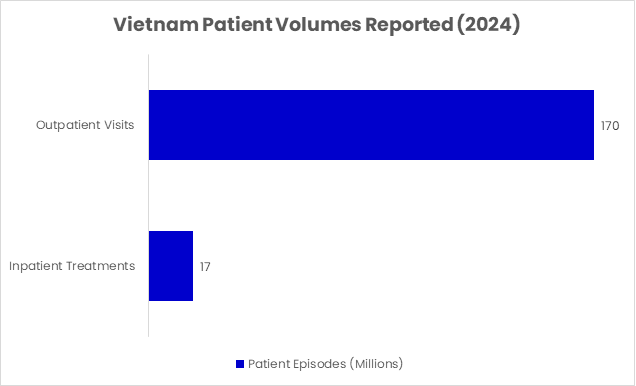

Figure 4: Vietnam reported more than 170 million outpatient visits and over 17 million inpatient treatments in 2024, highlighting the scale difference between frequent outpatient touchpoints and lower-frequency hospitalization. Source: VietnamPlus.

Healthcare demand in Vietnam is not only growing; it is frequent. The same VietnamPlus review reported more than 170 million outpatient visits and over 17 million inpatient treatments in 2024. Most patient interactions happen outside hospitalization, so the investable market is not limited to owning beds. It includes consultations, screening, diagnostics, pharmacy coordination, telehealth follow-up, and specialist referral.

This is where private providers can be especially strong. Consumers do not always choose a private facility because they need the most complex treatment. They often choose it because the process is easier: after-work paediatrics, same-day imaging, clearer lab explanations, or consistent follow-up for chronic conditions.

The economic logic is similar to modern retail and financial services: the provider that controls the customer relationship can expand wallet share. A clinic that begins with paediatrics can add vaccination, nutrition, diagnostics, dental, and family medicine. A specialty brand can extend from treatment to screening and post-treatment care.

However, this creates a new standard for execution. Healthcare platforms need more than marketing. They need clinical protocols, transparent pricing, data security, regulatory discipline, complaint handling, and medical leadership. Patient trust is slow to build and fast to lose. This is why institutional capital must be paired with operator discipline, not only expansion funding.

The Care Economy Is Broader Than Hospitals

Chronic Disease, Prevention and Elder Services Are Expanding the Addressable Market

Vietnam’s care economy is being shaped by disease burden as much as by income. The U.S. International Trade Administration, citing WHO data, noted that non-communicable diseases account for about 74% of total deaths in Vietnam. That changes the care model. Chronic conditions require earlier detection, regular monitoring, medication adherence, lifestyle support, and specialist coordination. They are not solved by a single hospital visit. This creates a strong case for preventive and outpatient care. Screening packages, cardiology diagnostics, diabetes management, cancer detection, women’s health, ophthalmology, and mental health services become more relevant as households move from reactive treatment to risk management. Employers can also become buyers through annual health checks and benefits programs.

Eldercare is the next frontier, although it may develop more slowly. Vietnam’s family structure still absorbs much of the elderly-care burden, but urbanization, smaller households, overseas migration, and dual-income families will make informal care harder to sustain. The opportunity may begin with day-care services, home nursing, rehabilitation, physiotherapy, mobility support, and chronic disease monitoring rather than Western-style nursing homes.

Private insurance and health-tech can support the market, but they are not magic solutions. Insurance penetration can help households pre-pay for care, while digital tools can reduce booking friction and improve patient records. Still, Vietnam’s healthcare opportunity remains fundamentally operational. The winners will be providers that combine medical credibility, convenient access, clean facilities, transparent payment flows, and disciplined unit economics.

Capital Stack Fit: Strategic Buyers, Private Equity and Credit

Private healthcare can fit several investor types. Strategic healthcare groups may seek geographic expansion or Vietnam entry through joint ventures and acquisitions. Private equity can back platform consolidation in diagnostics, clinics, hospitals, and elderly services. Private credit can support equipment purchases and facility upgrades where cash flows are visible but bank financing is conservative. The strongest targets will not necessarily be the largest. In healthcare, mid-sized assets with strong local reputation, repeat patients, doctor loyalty, clean licensing, and expansion-ready systems may be more valuable than bigger assets with weak governance. Investors should underwrite doctor concentration, revenue mix, payer mix, referral sources, equipment utilization, compliance history, and patient retention.

There is also a real estate angle. Medical facilities need accessible locations, parking, residential catchments, and compliance-ready buildings. But unlike ordinary real estate, healthcare value is created by the operating license, medical team, brand, and service model. In M&A terms, healthcare requires patient capital. Integration is slower than in many consumer sectors because clinical processes, staff incentives, and patient trust cannot be forced. The best consolidation strategies will likely be phased: acquire a credible anchor, standardize systems, add adjacent services, strengthen referrals, and expand geographically only after the operating model is stable.

Risks and Structural Headwinds

Trust, Talent and Regulation Define the Downside Case

The opportunity is real, but healthcare is unforgiving. The first risk is clinical trust. A logistics delay or retail stockout damages service quality; a medical error can damage lives, reputation, and licensing. Investors must treat governance, medical protocols, and quality assurance as core value drivers rather than back-office costs.

The second risk is talent. Doctors, nurses, technicians, pharmacists, and administrators are the productive capacity of a healthcare platform. Expansion without staffing depth can dilute service quality. A clinic chain that grows faster than its ability to recruit and train medical teams may lose the very trust it is trying to monetize.

The third risk is affordability. Vietnam’s high out-of-pocket spending creates private demand, but it also limits pricing. World Bank data show out-of-pocket expenditure was about 39.2% of current health expenditure in 2023. The durable model is not luxury care for a small elite, but accessible premium care for a broad middle-income population.

Regulation is another key variable. Healthcare licensing, foreign ownership structures, advertising rules, insurance reimbursement, drug distribution, medical equipment standards, and data privacy can all affect growth. Professional operators may benefit from stricter standards over time, but compliance costs must be built into the model from the beginning.

Closing Perspective: Vietnam’s Next Essential Services Platform

Vietnam’s private healthcare opportunity is not a short-term consumer trend. It is a structural response to ageing, rising incomes, chronic disease, public-system pressure, and household demand for better service. The country’s care economy is moving from fragmented providers toward more organised platforms that can deliver consistent quality across repeated patient interactions.

The investment case is strongest where healthcare behaves like essential infrastructure with consumer-facing quality: diagnostics, outpatient specialties, family medicine, rehabilitation, preventive care, elder services, and selective hospital platforms. These models can build recurring relationships, capture rising health spending, and support consolidation in a fragmented market.

The challenge is execution. Healthcare platforms cannot be scaled like ordinary roll-ups. Investors need clinical governance, talent strategy, compliance discipline, and patient trust. But for capital that can combine operational patience with institutional systems, Vietnam’s care economy may become one of the country’s most important long-term investment themes.

For deeper insights on capital markets, infrastructure investment, healthcare platforms, and emerging market opportunities, follow DealFlow for research-driven perspectives on global finance via LinkedIn or explore further analysis at DealFlow.sg.