Southeast Asia’s economic story is frequently told through its export prowess, its digital economy surge, and the rise of its consumer class. Yet beneath these headline narratives lies a persistent and largely underreported structural failure: a deep, systemic mismatch between the capital needs of the region’s mid-market businesses and the supply of financing available to them. Across Indonesia, Vietnam, the Philippines, Malaysia, and Thailand, tens of thousands of commercially viable companies find themselves stranded in a financing no-man’s land — too large for microfinance, too informal or too small to satisfy the rigid underwriting criteria of domestic commercial banks, and too unfamiliar with capital markets to access debt instruments independently.

This financing void is not a temporary market inefficiency. It is a structural gap rooted in the architecture of Asian financial systems, where bank-dominated credit markets have long prioritized investment-grade credits and collateral-heavy borrowers. Into this gap, private credit is rapidly emerging as the most compelling institutional solution — offering bespoke, flexible, and relationship-driven financing that neither banks nor equity markets are equipped to provide. The question for sophisticated capital allocators is no longer whether private credit in Southeast Asia will grow, but how quickly and who will capture the most defensible positions.

The Evolution of Southeast Asia’s Credit Landscape

Bank Dominance and Its Structural Limits

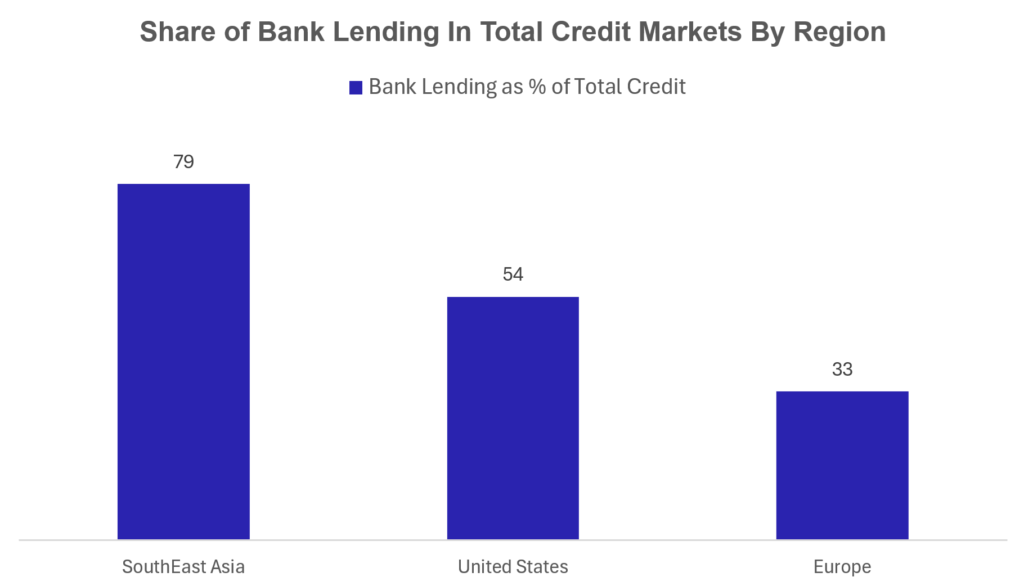

Figure 1: Bank lending dominates Southeast Asia’s credit mix at 79%, versus 54% in Europe and 33% in the US — leaving a vast structural opening for private credit to fill.

Southeast Asia’s financial systems are overwhelmingly bank-centric by global standards. Across the region’s major economies, commercial banks account for approximately 79% of total lending activity — a figure that stands in sharp contrast to Europe (54%) and the United States (33%), where non-bank credit markets are substantially more developed. This extreme bank concentration reflects decades of regulatory frameworks that privileged deposit-taking institutions, suppressed non-bank competition, and left alternative capital channels structurally underdeveloped.

The consequence of this architecture is predictable: commercial banks, operating within conservative Basel III and local prudential frameworks, have systematically retreated from the mid-market. As risk appetite has narrowed, banks have concentrated their loan books on top-tier investment-grade corporates and government-linked entities. The mid-market borrower — typically generating revenues between USD 5 million and USD 100 million, with genuine growth prospects but limited formal credit history — is effectively invisible to conventional lenders.

The Retreat of Conventional Lending and the Structural Opening

The withdrawal of bank credit from the mid-market has accelerated meaningfully since 2022. Rising global interest rates forced Asian banks to tighten underwriting standards and reduce exposure to unrated credits. Simultaneously, the collapse of Asia’s high-yield public bond market — driven by a wave of Chinese real estate defaults and a broader investor retreat from Asian credit risk — eliminated another financing channel that mid-market borrowers had intermittently accessed. According to senior bankers at JPMorgan, the public high-yield market in Asia effectively closed for most mid-market issuers over the 2022 to 2024 period, accelerating demand for private financing solutions.

Against this backdrop, private credit funds have moved decisively to fill the void. These non-bank lenders offer what banks cannot: speed of execution, structuring flexibility, covenant customization, and willingness to engage with complex or non-standard financing scenarios. For Southeast Asian borrowers unaccustomed to the institutional capital ecosystem, private credit funds also provide something intangible but equally important — a long-term financing partner willing to build genuine relationships over multiple capital cycles.

A Market Abundant in Borrowers, Deficient in Solutions

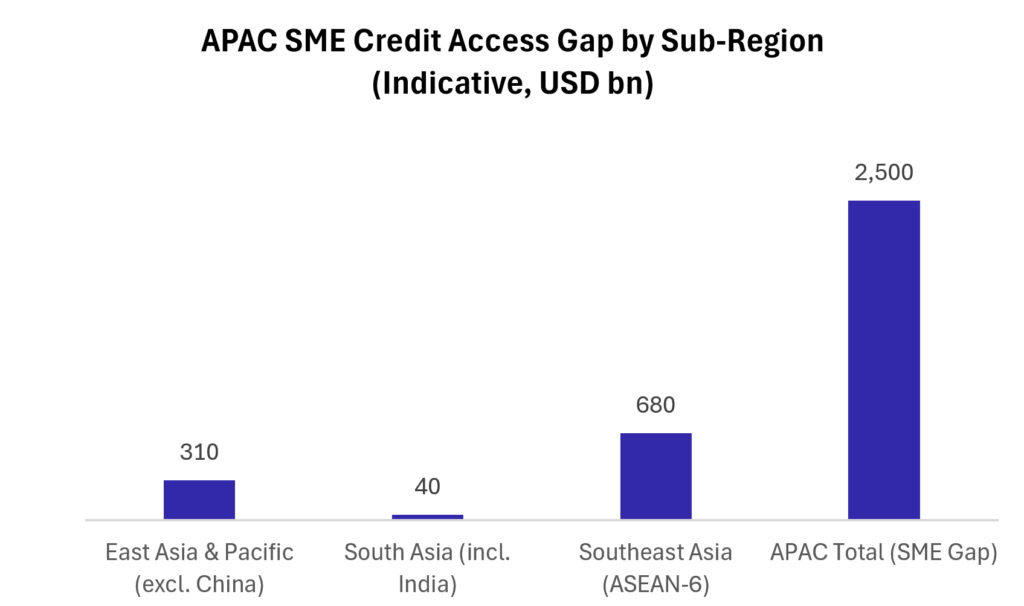

The scale of the financing gap in Southeast Asia is difficult to overstate. SMEs account for over 97% of all enterprises across the region’s major economies and collectively contribute between 40% and 60% of GDP in markets such as Indonesia, Vietnam, and the Philippines. Yet despite this economic centrality, SME financing accounts for only 22% of total bank loans in APAC’s developing economies, according to the Asian Development Bank. Asia as a whole faces a USD 2.5 trillion credit access gap for small and medium enterprises — more than half of the global financing shortfall for this segment.

At the macro level, the region’s aggregate infrastructure financing gap alone stands at USD 1.7 trillion annually for emerging Asia (excluding China), according to AIMA data, with renewable energy, digital infrastructure, and transportation representing the most capital-intensive needs. Private credit is uniquely positioned to address both segments — scaling mid-market corporate lending while simultaneously unlocking long-duration infrastructure financing that sits beyond the appetite of both banks and short-duration equity funds.

The Emergence of Private Credit as an Institutional Asset Class

Defining the Opportunity

Private credit — broadly defined as privately negotiated loans between non-bank lenders and borrowers — encompasses several distinct sub-strategies relevant to Southeast Asia. Direct lending to mid-market corporates and sponsor-backed buyouts forms the largest and fastest-growing segment, targeting companies seeking term financing without the constraints of public debt covenants. Mezzanine and junior debt structures serve borrowers at the complex end of the capital stack, while specialty finance vehicles address asset-backed lending, supply chain financing, and sector-specific receivables. Distressed and special situation lending — a less developed but growing segment in the region — is beginning to attract dedicated capital as credit cycles normalize and non-performing loans accumulate in certain markets.

For Southeast Asian borrowers, the specific appeal of private credit lies in its operational compatibility. Repayment schedules can be structured around actual cash flow cycles rather than standardized amortization templates. Covenant packages can be tailored to reflect sector-specific operating realities. Drawdown flexibility allows borrowers to access capital as project milestones are achieved, rather than receiving a lump-sum disbursement that must be immediately deployed. These features are not merely preferences — for many mid-market borrowers in the region, they represent the difference between accessing capital and being entirely shut out of the institutional financing system.

Why Global Capital Is Moving Into the Region

The most consequential macro force driving private credit into Southeast Asia is the relative saturation of Western markets. Global private credit assets under management reached USD 3 trillion in 2024, with the United States and Europe absorbing the vast majority of that capital. The result is intense spread compression in developed markets, where large-cap direct lending transactions now command yields that have converged meaningfully toward leveraged loan rates. Sophisticated managers seeking yield enhancement and portfolio diversification are systematically pivoting their geographic allocation frameworks toward Asia.

Southeast Asia, in particular, offers what mature markets cannot: a genuine spread premium above comparable Western credits, structural growth dynamics driven by demographics and urbanization, and a borrower universe that has not yet been fully institutionalized. As Temasek’s formation of a SGD 10 billion private credit entity in late 2024 demonstrated, even the most sophisticated institutional capital in the world is now explicitly targeting this structural gap. Apollo Global Management’s appointment to manage Singapore’s USD 1 billion private credit mandate for high-growth businesses underlines the same conviction from global alternative managers.

AUM Growth and Market Momentum

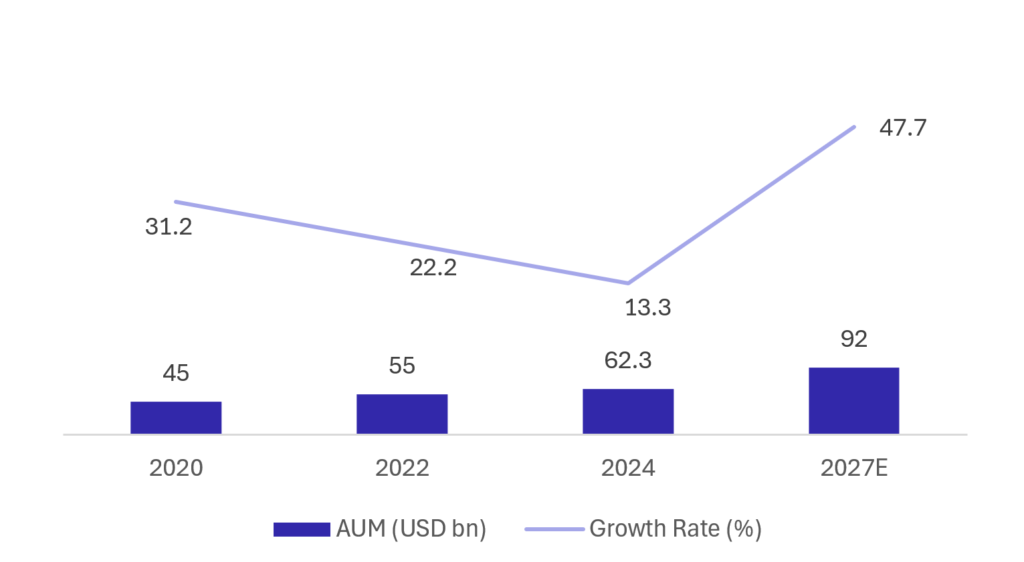

Figure 2: APAC private credit AUM is projected to nearly triple from its 2017 base, reaching USD 92 billion by 2027 — with Southeast Asia as the fastest-growing sub-region.

The quantitative evidence for private credit’s ascent in Asia Pacific is unambiguous. Private credit AUM in the region grew from virtually zero in 2000 to USD 34.3 billion in 2018, before more than doubling to USD 62.3 billion by the first quarter of 2024. According to the Alternative Investment Management Association (AIMA), APAC private credit AUM is forecast to reach USD 92 billion by 2027, implying a compound annual growth rate of 16% from 2024 levels. Fundraising for Asia-focused private credit funds outperformed 2024 levels significantly in 2025, with notable late-year closes anchoring a strong full-year result.

Southeast Asia specifically is emerging as the primary beneficiary of intra-regional capital reallocation. According to the EY Southeast Asia Private Equity Pulse 2025, private credit is set for accelerated growth in 2026, driven by sustained demand from mid-market corporates and financial sponsors operating in tightening bank lending conditions. Rising allocations from local pension funds and insurance companies, alongside growing cross-border appetite for unitranche and mezzanine structures, are systematically deepening market liquidity and capability.

Structuring as the Primary Differentiator in Asian Credit Markets

The single greatest misconception about private credit in Southeast Asia is that it competes primarily on price. It does not. Traditional commercial bank loans in the region typically cost 200 to 400 basis points less than comparable private credit facilities. Any fund entering the market expecting to win on rate will fail systematically. The true competitive advantage of private credit lies in structural customization — the ability to construct financing solutions that match the operational tempo and capital deployment rhythm of each individual borrower.

In practice, this manifests across several distinct structuring dimensions. At the term level, private credit managers can extend tenors to three to seven years, providing genuine planning certainty that revolving bank facilities cannot offer. At the structure level, unitranche arrangements — which combine senior and junior debt into a single instrument — simplify the borrower’s capital stack and eliminate intercreditor complexity. Payment-in-kind (PIK) features allow interest to accrue rather than be paid currently, preserving cash flow during growth-intensive capital deployment phases. Covenant packages can include maintenance-free provisions or capped financial covenant tests calibrated to the actual operating cycle of the underlying business.

For capital allocators, the structuring imperative runs in parallel. Successful private credit managers in Southeast Asia combine deep credit underwriting capability with genuine sector expertise. A lender financing a healthcare services platform in Indonesia must understand reimbursement dynamics, licensing frameworks, and patient acquisition economics — not merely the borrower’s EBITDA coverage ratio. This requirement for operational depth effectively raises the barrier to entry for generalist managers and creates sustainable competitive moats for specialists with embedded regional networks.

Key Risks and Structural Headwinds

The opportunity in Southeast Asia private credit is real and substantial. But it is not without meaningful risk, and the most sophisticated participants approach the market with a clear-eyed assessment of the structural headwinds that will separate disciplined managers from opportunistic capital.

The Borrower Education Gap and Execution Complexity

Perhaps the most underestimated risk in the region is the depth of the borrower education gap. For the vast majority of Southeast Asian mid-market business owners, private credit is not merely unfamiliar — it is genuinely foreign as a concept. Most entrepreneurs associate debt financing exclusively with commercial bank loans and view non-bank lending with suspicion, associating it with informal grey market lenders or predatory structures. Overcoming this perception requires sustained relationship investment, transparent communication, and the demonstrated willingness to structure transactions that genuinely align lender and borrower incentives.

Regulatory complexity compounds the execution challenge. Credit licensing regimes vary dramatically across the region’s major markets. Indonesia, Vietnam, Malaysia, and the Philippines each maintain distinct frameworks governing non-bank lending activity, foreign capital participation in domestic credit markets, and enforcement rights over collateral and guarantees. Cross-border transactions must navigate multiple legal jurisdictions simultaneously, requiring specialist legal counsel and deep regulatory familiarity. For global managers entering the region for the first time, these barriers are not trivial — underestimating them is a reliable route to expensive operational failures.

Figure 3: Asia’s SME financing gap reaches USD 2.5 trillion across the region, with Southeast Asia representing the most acute concentration of unmet demand relative to GDP.

Currency risk represents a further structural consideration that is frequently underpriced by global allocators entering the region. Private credit transactions denominated in local currencies — Indonesian rupiah, Vietnamese dong, or Philippine peso — expose foreign investors to exchange rate volatility that can materially alter USD-equivalent returns. Hedging instruments exist for the major regional currencies but are costly and imperfect in their coverage. The most experienced regional managers either operate through local currency fund structures, incorporate robust hedging programs into their fund architecture, or accept USD-denominated lending exclusively — each approach carrying its own trade-offs.

From Isolated Lending to Platform Capital

The long-term vision for private credit in Southeast Asia extends well beyond individual loan transactions. The most sophisticated managers are building platform lending businesses — deploying capital across a coherent sector thesis, accumulating proprietary underwriting data, and establishing the origination networks that allow them to see the best transactions before they become competitive processes.

Sector Concentration and the Path to Scale

The sectors attracting the greatest private credit attention in Southeast Asia reflect a clear structural logic. Digital infrastructure — encompassing data centres, telecom towers, and fibre networks — generates long-duration contracted cash flows that align naturally with private credit’s investment horizon. Healthcare services represent a demographically driven growth sector with inherently stable revenue streams and significant capital requirements for facility expansion and equipment financing. Renewable energy projects, particularly solar and wind developments across Vietnam, Indonesia, and the Philippines, offer government-contracted revenue certainty and asset-backed security profiles that traditional banks have been slow to embrace. Logistics and cold chain infrastructure, turbo-charged by the region’s booming e-commerce sector, presents a further avenue for asset-backed lending with predictable utilization economics.

Buy-and-build strategies in fragmented sectors are also emerging as a significant source of private credit demand. As private equity managers execute consolidation strategies across healthcare, education, and consumer services — aggregating founder-led businesses into institutional platforms — they increasingly require flexible debt capital to finance each individual acquisition. Private credit funds are ideally positioned to serve as the primary capital provider in these leveraged buyout and add-on acquisition structures, combining senior term debt, acquisition bridge facilities, and working capital revolvers into integrated financing packages.

Implications for Capital Allocators

Key Signals to Monitor

Over the coming investment cycle, the most compelling private credit entry points in Southeast Asia will be defined by the intersection of three conditions: genuine borrower quality, demonstrable collateral or cash flow predictability, and a sector tailwind that is fundamentally driven by domestic demand rather than export-cycle dependency. Capital allocators should systematically track the evolution of non-performing loan ratios in regional banking systems, as deteriorating bank asset quality tends to accelerate the retreat from mid-market lending and expand the opportunity set for private credit. Regulatory developments across Indonesia’s OJK, Vietnam’s State Bank, and the Philippines’ BSP warrant close monitoring — licensing reforms that expand the operating scope for non-bank credit providers will catalyze a step-change in market depth.

Investor composition within the region is also shifting in ways that carry strategic implications. Rising allocations from ASEAN pension funds and domestic insurance companies are beginning to build a local institutional base for private credit that reduces dependence on cross-border capital flows. This deepening of the domestic investor base is structurally important — it diversifies the LP register, reduces currency risk at the fund level, and insulates the market from global risk-off episodes that historically caused abrupt capital withdrawals from Asian emerging markets.

Who Is Best Positioned to Win

The structural dynamics of Southeast Asia’s private credit market systematically advantage a specific category of capital allocator. Managers with dedicated regional infrastructure — on-the-ground origination teams, established borrower relationships across multiple markets, and deep sector expertise in the region’s highest-growth industries — will generate deal flow and underwriting quality that global generalists cannot replicate. Long-duration capital structures, such as evergreen fund vehicles or closed-end funds with extended seven to ten-year investment periods, are better matched to the patient relationship-building required to originate and execute in the region than short-cycle funds chasing rapid deployment.

Equally important is genuine operational capability beyond the credit agreement. The best private credit managers in Southeast Asia act as genuine financing partners — connecting borrowers to procurement networks, facilitating introductions to equity co-investors, and providing governance guidance that helps companies strengthen their institutional readiness over the life of the investment. This value-added orientation is not altruism; it is a direct risk management tool. A borrower that grows stronger operationally during the credit period is substantially less likely to experience covenant stress or default, and is far more likely to become a repeat client as the relationship matures.

Closing the Gap: The Private Credit Imperative in Southeast Asia

Southeast Asia stands at a critical inflection point in its financial market development. The structural conditions for a durable private credit expansion are firmly in place: a USD 2.5 trillion SME financing gap that banks are systematically failing to address, a borrower universe that is commercially sophisticated but institutionally underserved, and a global capital base actively seeking yield, diversification, and exposure to the region’s structural growth dynamics. The APAC private credit market’s trajectory from USD 34 billion in 2017 to a projected USD 92 billion by 2027 reflects not a speculative bubble but a legitimate and durable structural rebalancing of Asia’s credit markets.

For capital allocators equipped with the patience, the regional expertise, and the structuring capability to navigate this landscape, the opportunity is generational. The most defensible returns will accrue not to those who merely deploy capital at scale, but to those who build the origination relationships, the underwriting depth, and the operational partnerships that convert Southeast Asia’s vast pool of creditworthy but underserved borrowers into institutional-grade private credit assets. At the intersection of structural scarcity, demographic growth, and financial system maturation, private credit in Southeast Asia represents one of Asia’s most compelling and durable capital allocation opportunities of the coming decade.

For deeper insights on capital markets, infrastructure investment, and emerging market opportunities, follow DealFlow for research-driven perspectives on global finance via LinkedIn or explore further analysis at Dealflow.sg.