Vietnam’s economic rise has been defined by manufacturing scale, export competitiveness, and sustained foreign direct investment. As the country approaches middle-income maturity, its next phase depends on financial sophistication: mobilizing savings, attracting institutional capital, pricing risk, and converting corporate growth into investable financial assets. The Vietnam International Financial Centre in Ho Chi Minh City is a deliberate attempt to build this next layer of national competitiveness.

VIFC-HCMC is not simply a real estate project or branding exercise. It is an institutional architecture intended to reposition Ho Chi Minh City from a domestic commercial centre into a regional platform for capital formation, asset management, fintech experimentation, and cross-border financial services. The key question is whether Vietnam can translate ambition into legal certainty, infrastructure, and human capital.

The Evolution of Vietnam’s Financial Landscape

Bank Dominance and Its Structural Limits

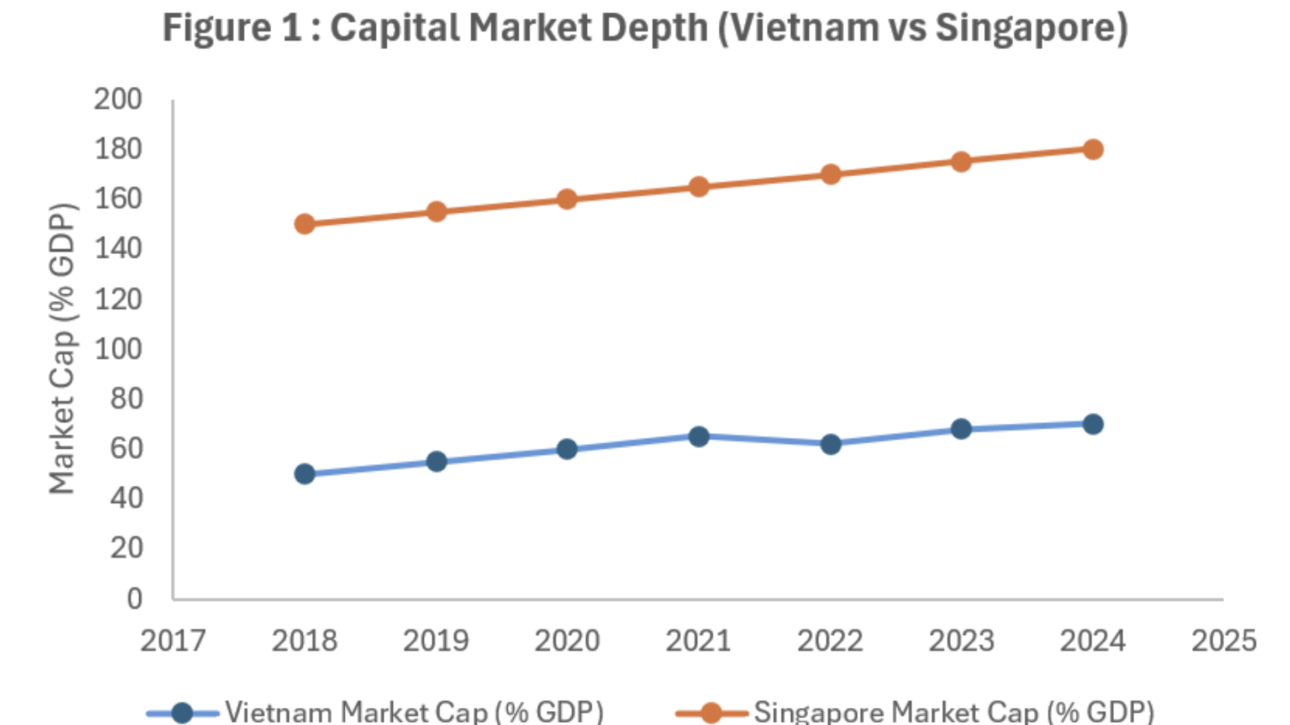

Looking at Figure 1, Vietnam’s capital market depth remains materially below Singapore’s, highlighting the structural upside from deeper equity, bond, and institutional capital markets.

Vietnam’s financial system remains bank centric. Credit allocation has historically been led by domestic commercial banks, with credit-to-GDP ratios exceeding 120% in recent years, while equity market capitalization and corporate bond depth remain less developed. This model supported industrialization, but also created concentration risk, maturity mismatches, and limited financing channels for businesses needing more sophisticated capital solutions.

The result is an imbalance between economic growth and financial intermediation. Many strong Vietnamese companies still rely on collateral-heavy bank loans, shareholder funding, or offshore structures. Debt markets, institutional investors, derivatives, securitization, and professional asset management remain underdeveloped. The VIFC-HCMC framework targets this gap by creating an ecosystem where domestic and cross-border capital can be raised, managed, priced, and recycled more efficiently.

From Financial Periphery to Regional Node

Vietnam has integrated successfully into global supply chains, but its financial system has not captured the full value of that integration. Large exporters, consumer champions, infrastructure developers, and technology firms increasingly operate across borders, yet many still depend on offshore jurisdictions. This creates value leakage in advisory fees, fund domiciliation, legal structuring, and capital markets activity that could eventually be localized.

VIFC-HCMC is designed to address this disconnect. Ho Chi Minh City already functions as Vietnam’s commercial nerve centre. By layering specialized financial regulations, tax incentives, dispute resolution, and global connectivity onto this base, Vietnam is moving from financial periphery to regional node. The goal is to capture more Vietnam-linked capital activity and become a credible ASEAN platform.

A Market Rich in Economic Growth, Deficient in Capital Intermediation

Vietnam’s opportunity lies in the mismatch between real-economy expansion and financial-market sophistication. Manufacturing relocation, urbanization, rising household wealth, digital adoption, and infrastructure demand are creating more companies, projects, and investors that need more than bank credit. IPOs, bonds, private equity exits, green finance, wealth management, and structured products become increasingly relevant as the economy grows more complex.

Yet the domestic financial system has not fully evolved. Capital markets remain shallow, institutional investors are developing, and foreign investors face frictions around access, reporting, currency convertibility, and dispute resolution. The VIFC-HCMC blueprint seeks to create a more investable environment where international capital can enter with confidence, domestic savings can be professionally managed, and Vietnamese enterprises can access growth-aligned financing structures.

The Emergence of VIFC-HCMC as an Institutional Platform

Defining the Opportunity

The VIFC-HCMC should be understood as a platform rather than a single institution. It is intended to connect functions currently fragmented across domestic and offshore channels: capital markets, asset and fund management, banking and fintech, niche financial markets, green finance, and professional services. If executed effectively, the centre could convert Vietnam’s corporate growth story into institutional-grade financial products.

For investors, the appeal is proximity to a high-growth economy still underpenetrated by sophisticated capital solutions. A VIFC-based ecosystem could support IPO preparation, cross-border bond issuance, fund management, private market vehicles, and alternative financing. For domestic businesses, the value is access to broader capital sources without relying solely on banks or moving complex financing offshore.

Why Global Capital Is Paying Attention

Global capital is searching for growth markets that combine macro momentum with improving institutional quality. Vietnam already offers manufacturing competitiveness, demographics, and consumption. The VIFC aims to strengthen the institutional side through rules, infrastructure, and professional capabilities. For asset managers, private equity firms, pension funds, and sovereign investors, growth is not enough without credible entry, governance, exit, and dispute resolution.

The initiative also reflects a regional trend. Asian financial centres now compete on regulatory clarity, talent depth, product innovation, and connectivity. Singapore and Hong Kong remain far ahead, but Vietnam’s strategy is tied to an expanding domestic economy. If HCMC can offer a gateway to Vietnamese deal flow, infrastructure finance, green transition projects, and consumer growth, it can occupy a complementary position.

Market Momentum and Institutional Readiness

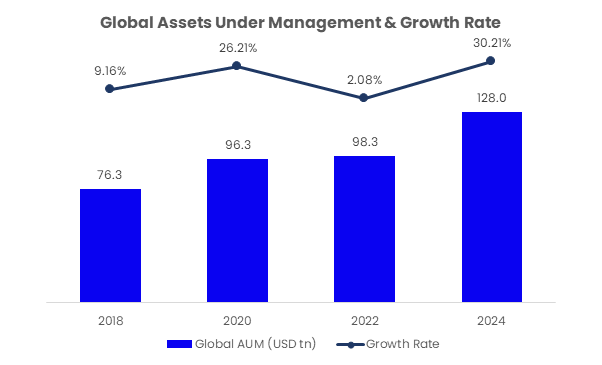

Figure 2: Global Assets Under Management Growth

As Figure 2 shows, global assets under management expanded from USD 76.3 trillion in 2018 to USD 128.0 trillion in 2024, underscoring the scale of capital pools that financial centres compete to attract. Growth has not been linear: after a sharp expansion between 2018 and 2020, global AUM growth slowed to just 2.1% between 2020 and 2022, before rebounding strongly to 30.2% between 2022 and 2024. This volatility highlights why investors and asset managers increasingly value jurisdictions with credible regulation, efficient fund structures, and institutional depth.

The quantitative case for the VIFC is therefore anchored in Vietnam’s ability to position itself within this expanding global capital pool. While global AUM has reached record levels, Vietnam still captures only a limited share of international asset management activity relative to its economic growth potential. At the same time, the domestic savings base is expanding as household wealth rises, listed markets deepen, and insurers and institutional investors become more relevant. A credible HCMC asset management framework could help connect both domestic and international capital to Vietnam-linked opportunities.

Institutional readiness will determine whether this opportunity becomes durable. Asset managers require tax neutrality, clear fund structures, reliable reporting, enforceable contracts, and efficient capital repatriation. The VIFC’s proposed international accounting standards, English-language documentation, and specialized dispute resolution mechanisms will therefore shape whether global managers treat Vietnam merely as a sourcing market, or as a genuine platform for regional capital allocation.

Governance as the Primary Differentiator in Financial Centre Competition

The biggest misconception about building a financial centre is that physical infrastructure is decisive. Modern financial centres compete primarily on governance: legal certainty, regulatory coherence, tax clarity, enforceability, and operational speed. Office districts create visibility, but cannot substitute for trust. For VIFC-HCMC, governance separates a policy announcement from a functioning ecosystem.

This challenge spans several dimensions. The centre must offer a regulatory perimeter flexible enough for innovation but disciplined enough to avoid reputational risk. It must coordinate across ministries, regulators, tax authorities, and local government bodies without contradictory rules. It must also provide predictable dispute resolution and align reporting with global expectations through IFRS-based practices.

This is why legal autonomy is central to the VIFC blueprint. Specialized rules allowing English-language transactions, international accounting practices, and controlled experimentation are credibility signals. The more the VIFC reduces execution friction and legal uncertainty, the more likely it is to attract serious institutions rather than short-term regulatory arbitrage.

Key Risks and Structural Headwinds

The opportunity for VIFC-HCMC is real, but not guaranteed. Financial centres are difficult to engineer because they require alignment among policy, market demand, institutional trust, professional talent, and international perception. Vietnam has the economic momentum to justify the ambition, but execution risks remain material.

The Execution Gap and Regulatory Complexity

The most immediate risk is the execution gap between policy design and market implementation. Investors will judge the VIFC by practical experience: approval timelines, dispute handling, tax interpretation, and regulatory consistency. Even small ambiguities can reduce confidence when institutions decide where to domicile funds or establish regional teams.

Regulatory complexity compounds this challenge.

A financial centre requires coordination across securities regulation, banking supervision, tax policy, foreign exchange rules, corporate law, fintech licensing, and anti-money laundering standards. If these areas move at different speeds, the ecosystem can fragment. The VIFC must avoid disconnected incentives and create a coherent operating environment that is transparent for global institutions and aligned with stability objectives.

Talent is another structural constraint. A financial centre is defined by fund managers, investment bankers, risk specialists, compliance officers, lawyers, accountants, and regulators. Vietnam faces shortages in many of these areas. Foreign professional incentives can help, but the longer-term test is whether imported expertise can be paired with domestic training to build a sustainable pipeline.

From Financial Infrastructure to Ecosystem Capital

The long-term vision for VIFC-HCMC extends beyond isolated transactions. Successful financial centres become ecosystems: dense networks of institutions, service providers, regulators, investors, and corporates. Vietnam’s goal should be a platform where capital formation becomes more efficient across the economy. Once credible institutions cluster in one location, deal flow, talent, and information begin to compound.

Sector Concentration and the Path to Scale

The sectors most likely to benefit from the VIFC reflect Vietnam’s development priorities. International capital markets can support IPOs, secondary offerings, and bond issuance. Asset and fund management can channel savings into private equity, infrastructure, real estate, and public markets. Digital banking and fintech can accelerate payments, lending, embedded finance, and tokenized assets. Aviation finance can leverage Vietnam’s aviation demand while building specialized expertise.

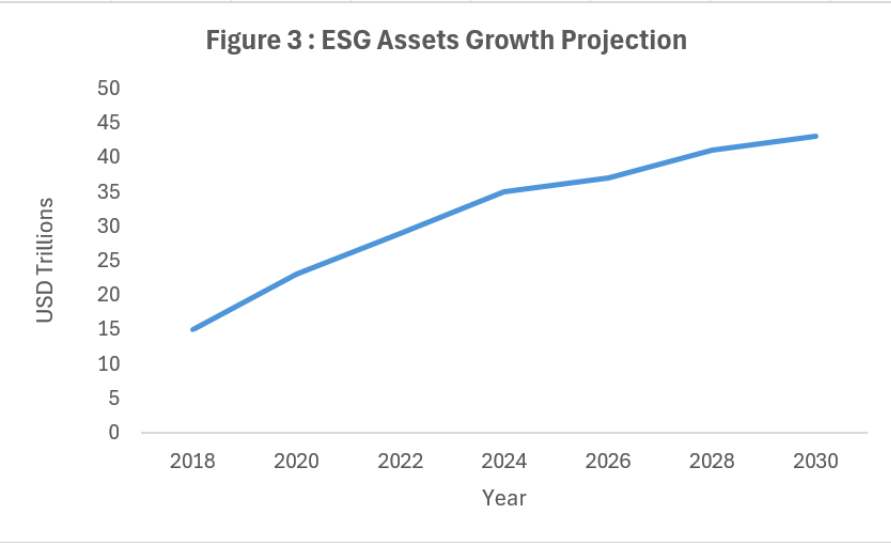

Figure 3: ESG Assets Growth Projection

As Figure 3 shows, global ESG assets are projected to expand from approximately USD 18 trillion in 2018 to more than USD 40 trillion by 2030, reflecting a major shift in how institutional capital is allocated. This matters because sustainability is not only a branding theme; it could become one of the VIFC’s most commercially relevant verticals.

Vietnam’s integration into export supply chains increasingly requires environmental compliance, including carbon accounting and transition planning. Carbon credit exchanges, green bond frameworks, and transition finance vehicles could help Vietnamese firms remain competitive while giving investors exposure to decarbonization opportunities. If structured credibly, green finance could become one of the VIFC’s most defensible niches.

Implications for Investors

Key Signals to Monitor

Investors should monitor whether the VIFC produces measurable increases in capital-market activity, not just headlines. Key indicators include IPO pipelines, corporate bond issuance, fund registrations, foreign asset manager participation, cross-border lending, fintech sandbox approvals, and professional services in HCMC. These signals will show whether the VIFC is becoming an operating platform or remaining a policy concept.

Investors should also track regulatory implementation: consistent tax incentives, workable foreign exchange and repatriation rules, credible dispute resolution, and clear regulator communication. A financial centre earns trust through repetition. Each successful fund launch, bond issuance, fintech pilot, or green finance transaction will matter more than broad strategy.

Who Is Best Positioned to Win

The VIFC will advantage institutions that combine Vietnam exposure with institutional operating capability. Global asset managers, private equity firms, banks, securities firms, and professional service providers with on-the-ground teams will be better positioned than firms treating Vietnam as an occasional transaction market. Local institutions that upgrade governance, reporting, risk management, and product capability will also benefit.

Equally important are investors and advisors that bridge domestic opportunity with international standards. Vietnam’s best companies often need more than capital; they need preparation for institutional ownership, cleaner reporting, stronger governance, and cross-border networks. The biggest winners may be those who convert Vietnam’s growth into financeable, tradable, and institutionally credible assets.

Engineering Financial Maturity: The VIFC-HCMC Imperative

Vietnam stands at a critical inflection point. The conditions for a more sophisticated capital ecosystem are in place: rapid economic growth, a large corporate base, rising household wealth, infrastructure demand, green finance needs, and global capital seeking Asian growth exposure. The VIFC-HCMC blueprint is Vietnam’s most comprehensive attempt to convert these conditions into a functioning financial platform.

Success depends on execution rather than aspiration. Vietnam must build legal certainty, regulatory coordination, market infrastructure, and professional talent to earn confidence from capital providers. If the VIFC delivers, it can deepen Vietnam’s financial system and redefine the country’s regional role. If execution falls short, it risks becoming symbolic; if it succeeds, it can materially alter Vietnam’s capital formation trajectory.

For deeper capital-markets insights, follow Dealflow on LinkedIn or visit Dealflow.sg.