Vietnam’s economic narrative has been built on three pillars: manufacturing relocation, foreign direct investment inflows, and export-driven GDP growth. These foundations are real, well-documented, and increasingly well understood by global capital allocators. What remains less understood — and considerably less capitalised — is the credit infrastructure that serves the companies operating beneath the top tier of Vietnam’s economy.

State-owned enterprise lending, foreign-invested enterprise financing, and large-cap corporate bonds have received disproportionate institutional attention. The mid-market — companies generating between USD 5 million and USD 100 million in annual revenue — has largely been left to navigate a financing environment that is structurally inadequate for its stage of growth.

This gap is not incidental. It reflects the composition of Vietnam’s banking sector, the limited depth of domestic capital markets, and the absence of a mature private credit industry. As Vietnam’s economy and corporate sector become more sophisticated, the financing gap is becoming increasingly visible and consequential. For institutional investors, this creates a rare combination: an economy growing fast enough to generate demand, a credit market underdeveloped enough to offer meaningful yield premiums, and a regulatory environment gradually opening to more flexible financing solutions.

Vietnam’s Banking Sector: Deep in Deposits, Constrained in Credit Allocation

A Credit System That Leaves the Middle Underserved

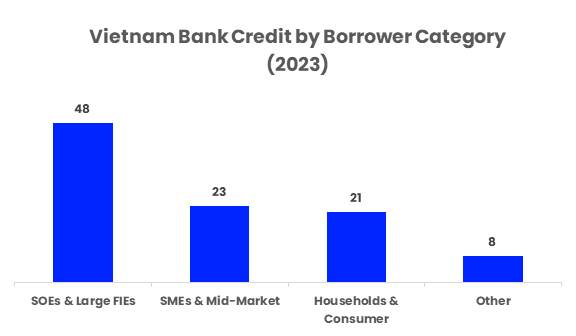

Figure 1: State-owned enterprises and large FIE corporates account for an estimated 45–50% of total Vietnamese bank credit outstanding, while SMEs and mid-market borrowers access approximately 20–25% despite representing over 97% of registered businesses. Source: State Bank of Vietnam, World Bank, 2023.

Vietnam’s banking system is large relative to the size of the economy. According to the State Bank of Vietnam (SBV), total domestic credit extended by the banking system reached approximately VND 13.6 quadrillion (roughly USD 554 billion) by end-2023, equivalent to around 116% of GDP — one of the highest credit-to-GDP ratios in Southeast Asia. On the surface, this suggests a credit-saturated economy. In practice, the distribution of that credit is severely skewed.

State-owned enterprises and large foreign-invested enterprises benefit from privileged access to bank lending, backed by implicit government guarantees, hard asset collateral, or the credit support of multinational parent companies. At the other extreme, household lending and micro-enterprise credit have been addressed through policy banks and microfinance channels. What remains underserved is the mid-market: companies large enough to have outgrown informal lending but too small, too young, or too lightly collateralised to consistently access bank credit on competitive terms. World Bank surveys of Vietnamese SMEs have consistently found that access to finance ranks among the top three constraints on business growth, and that collateral requirements — typically 120–150% of loan value in fixed assets — exclude a wide range of asset-light or growth-stage businesses.

Credit Quality Pressures Are Tightening Bank Lending Standards Further

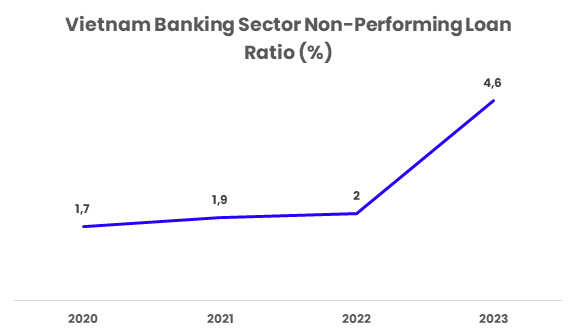

Figure 2: Vietnam’s reported NPL ratio rose from 1.7% in 2020 to 4.6% in 2023, contributing to tighter lending standards and more selective credit allocation. Source: State Bank of Vietnam, 2023.

The SBV’s non-performing loan resolution process has also made banks more conservative in mid-market credit extension. Reported NPL ratios across the Vietnamese banking system rose to approximately 4.6% of total loans by end-2023 according to SBV data, with some analysts estimating the true stressed-loan ratio — including restructured and watchlist exposures — closer to 7–9% of system assets. In this environment, credit committees are biased toward secured lending to established counterparties. Growth-stage companies, service-sector firms, and businesses without significant fixed-asset bases face higher rejection rates, longer processing times, and less favourable terms than their size and cash flow generation would justify in a more developed credit market.

The Size of the Financing Gap and Who It Affects

A Financial Gap Too Large for Banks Alone

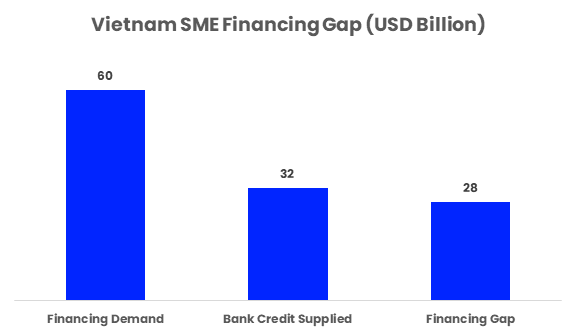

Figure 3: Vietnam’s SME financing demand is estimated at approximately USD 60 billion annually, with an estimated funding gap exceeding USD 28 billion due to limited access to traditional bank credit. Source: IFC SME Finance Gap Report.

Vietnam had approximately 900,000 active registered enterprises as of 2023, according to the General Statistics Office of Vietnam. While the overwhelming majority are micro and small businesses, the mid-market cohort — companies generating between USD 5 million and USD 100 million in annual revenue — represents a sizeable and increasingly important segment of the economy. IFC estimates place Vietnam’s SME financing gap at over USD 28 billion annually, reflecting substantial unmet demand from businesses that are unable to secure sufficient bank credit despite demonstrating viable growth prospects and operating cash flows.

The industries driving mid-market growth are varied but structurally compelling, spanning manufacturing suppliers to electronics and apparel multinationals, food processing and agricultural commodity businesses, domestic retail and distribution chains, logistics operators, healthcare providers, education services, and technology-enabled enterprises. Many of these businesses share similar characteristics: capital-intensive growth requirements, receivables-driven working capital cycles, limited fixed-asset collateral, and cash flow profiles that are well suited to debt financing but poorly aligned with traditional bank lending criteria.

The Public Bond Market Cannot Bridge the Gap

Vietnam’s domestic corporate bond market experienced rapid but unstable growth before a sharp correction. Gross corporate bond issuance peaked at approximately VND 650 trillion (USD 27 billion) in 2021, before collapsing to around VND 100 trillion in 2023 following a series of high-profile defaults and fraudulent issuances in the real estate sector, according to data from the Vietnam Bond Market Association (VBMA) and Hanoi Stock Exchange. Regulatory interventions — including Decree 65/2022 and its subsequent amendments — tightened disclosure requirements, investor eligibility criteria, and use-of-proceeds standards. While these reforms are structurally positive for market integrity, they have simultaneously made public bond issuance less accessible for mid-market companies that lack the legal resources, financial disclosure infrastructure, and investor relationships required to issue publicly at scale.

The Private Credit Opportunity: Yield, Structure, and Entry Conditions

Vietnam Offers Risk-Adjusted Premiums That Are Difficult to Replicate Elsewhere

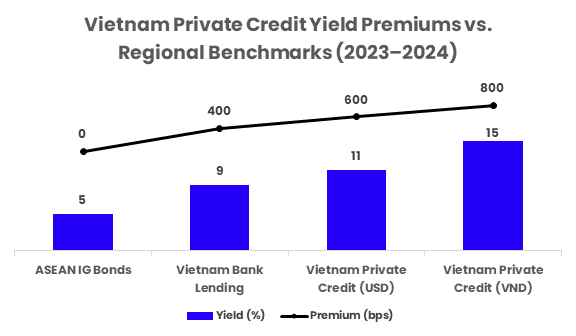

Figure 4: Indicative all-in yields for Vietnam private credit transactions ranged from approximately 8–13% in USD structures and 12–18% in VND structures during 2023–2024, representing a significant premium over both bank lending and regional public fixed-income alternatives. Source: DealFlow proprietary market intelligence, investor interviews, 2024.

For investors willing to accept illiquidity and operate with sufficient credit infrastructure, Vietnam’s private credit market offers yield premiums that are difficult to replicate in more developed regional markets. Indicative all-in returns on structured mid-market lending in Vietnam — combining interest income, arrangement fees, and structural protections — have ranged from 12–18% per annum in VND-denominated transactions and 8–13% per annum in USD-hedged or USD-denominated structures, depending on borrower quality, security package, tenor, and sector. These returns reflect genuine credit risk, not just illiquidity premium, and require careful borrower selection, legal structuring, and covenant monitoring.

The most attractive segments for private credit deployment include manufacturing supply chain financing — particularly receivables-backed lending to tier-two and tier-three suppliers of large multinationals — as well as growth capital for domestic consumer-facing businesses, project-level financing for logistics and industrial assets, and acquisition financing for regional consolidation strategies. In each case, the credit case rests on cash flow visibility, asset coverage, or customer concentration risk mitigation rather than on sponsor guarantees or government backing.

Legal and Structural Frameworks Are Evolving

One of the most significant constraints on Vietnam’s private credit market has been the legal and enforcement infrastructure around secured lending. Vietnamese law recognises several forms of collateral — real property, moveable assets, receivables, equity pledges — but enforcement has historically been slow, court capacity limited, and out-of-court resolution mechanisms underdeveloped. The introduction of Resolution 42 on NPL resolution in 2017 (extended in subsequent years) created a more workable framework for lender rights, and ongoing civil procedure reforms are gradually improving enforcement predictability. For private credit investors, this means that security structures can be built — but must be built with care, using local legal counsel with deep enforcement track records and preferably cross-border structural elements where USD-denominated instruments are involved.

Risks, Execution Challenges, and What Institutional Capital Requires

Information Asymmetry and Origination Are the Primary Barriers

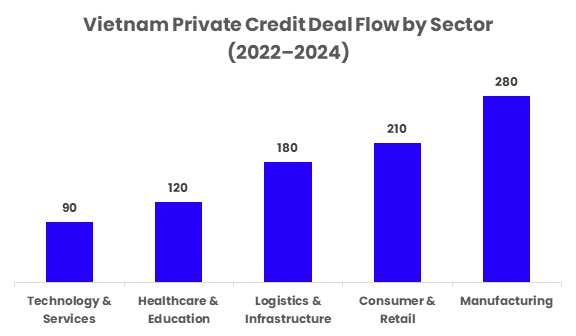

Figure 5: Manufacturing, consumer-facing businesses, and logistics-related companies accounted for the largest share of estimated private credit deployment in Vietnam between 2022 and 2024, reflecting sectors with strong cash-flow visibility and financing demand. Source: DealFlow proprietary market intelligence, investor interviews, 2024.

The barriers to scaling private credit in Vietnam are real. Information asymmetry is the most persistent: financial statements are frequently unaudited or prepared to local tax accounting standards rather than IFRS, related-party transactions are common and not always disclosed, and management projections are often optimistic relative to historical performance. Building conviction on a Vietnamese mid-market credit requires field-level due diligence — site visits, customer reference checks, supply chain verification, and independent financial reconstruction — that is resource-intensive and cannot be conducted remotely.

Origination is the second critical barrier. Vietnam’s mid-market does not have an established investment banking or advisory community that brings well-packaged credit opportunities to institutional lenders. Deal flow is relationship-driven, and building a reliable pipeline requires either a local presence or deep partnerships with accounting firms, law firms, trade associations, or sector-focused advisors with access to the right company networks. Investors entering the market through intermediaries without deep local relationships risk adverse selection — seeing only the deals that cannot be financed elsewhere.

Currency, Regulatory, and Concentration Risks

Currency exposure is a structural consideration for non-VND investors. The VND has depreciated against the USD by approximately 10–12% cumulatively over the 2020–2024 period, according to SBV and Bloomberg data. While hedging instruments are available for shorter tenors through Vietnamese commercial banks, the cost and availability of long-dated VND/USD hedges remain constraints. USD-denominated lending to Vietnamese borrowers partially mitigates currency risk but introduces mismatch risk for borrowers with VND revenue streams — a consideration that must be factored into debt sizing and covenant design.

Regulatory risk is also present. Vietnam’s legal framework governing foreign investment in financial instruments has evolved considerably, but restrictions on cross-border capital flows, limits on foreign ownership in certain sectors, and the evolving bond market regulatory environment all require ongoing monitoring. Investors must structure for the current environment while building flexibility for regulatory change — particularly as Vietnam advances its capital account liberalisation agenda in parallel with its aspirations for stock market reclassification from frontier to emerging market status.

Vietnam’s Private Credit Opportunity Is Structural, Not Cyclical

Vietnam’s mid-market financing gap is not a temporary artifact of tight monetary policy or post-pandemic caution. It is a structural feature of an economy that has grown faster than its credit infrastructure, in a banking system that was built to serve state priorities and has not fully reoriented toward private-sector mid-market needs. As the economy continues to grow — with GDP projected by the IMF to expand at 6.0–6.5% annually through 2028 — the financing demands of the mid-market will grow proportionally, and the gap will widen unless new capital channels are established.

Private credit is the most direct institutional response to this gap. It does not require Vietnam’s public markets to deepen further, does not depend on banking sector reform, and does not rely on government policy intervention. It requires investors with local knowledge, credit discipline, legal structuring capability, and the patience to build positions through relationship-driven origination. The returns available reflect these requirements — but they also reflect a genuine and durable market inefficiency that is unlikely to be competed away quickly.

For institutional capital seeking real yield, structural exposure to Vietnam’s growth, and diversification away from equity-market volatility, private credit represents the most direct and defensible entry point into one of Southeast Asia’s most compelling long-term economic stories.

For deeper insights on capital markets, private credit, and institutional investment across Southeast Asia, follow DealFlow for research-driven perspectives via LinkedIn or explore further analysis at DealFlow.sg.