The global allocation of capital to emerging markets has traditionally been framed through the lens of country risk. Political stability, sovereign creditworthiness, macroeconomic policy, and currency volatility have long served as the primary filters through which investors assess exposure to developing economies. In recent years, however, this framework has fundamentally shifted.

While macroeconomic and political considerations remain highly relevant, a growing body of evidence suggests that execution risk—rather than country risk alone—is increasingly dictating capital allocation across emerging Asia. Investors are less focused on where capital is deployed at the national level, and far more concerned with how reliably that capital can be converted into operating assets, cash flows, and long-term returns.

This shift reflects changing global investment conditions, tighter financial environments, and greater scrutiny of project-level outcomes. Capital is not retreating wholesale from emerging markets; rather, it is becoming far more selective in how it enters them. While execution risk is difficult to quantify directly, shifts in investment structures and sectoral allocations provide clear, observable proxies for how investors are pricing it today.

The Scale of Capital Deployment in Emerging Asia

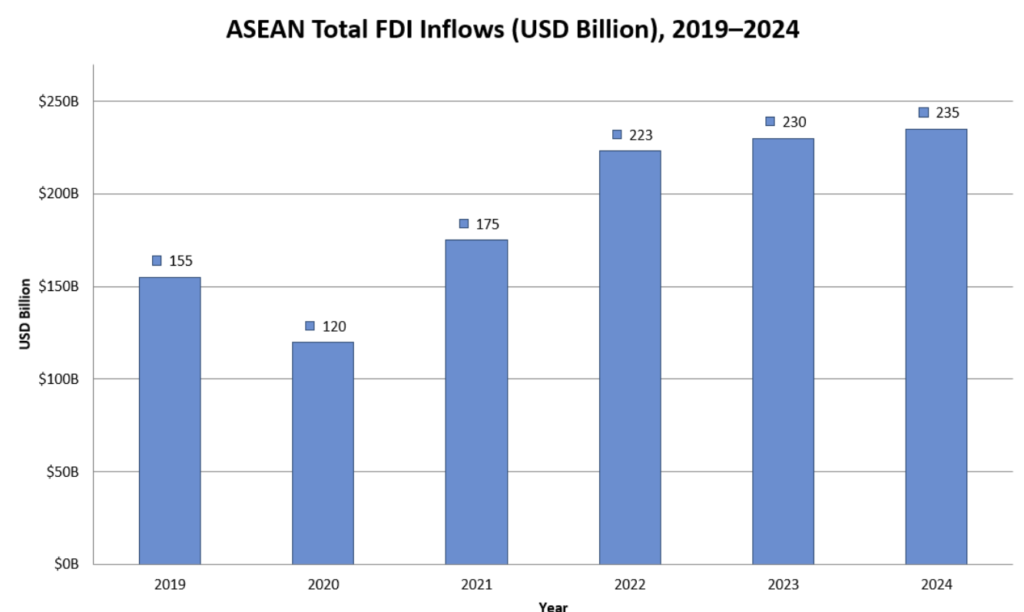

Emerging Asia continues to attract substantial volumes of foreign direct investment (FDI). According to UNCTAD, ASEAN economies collectively received approximately US$230 billion in FDI in 2023. This maintains the region’s position as a top recipient of global investment among developing regions, even amidst a broader worldwide slowdown. However, headline inflow figures obscure a meaningful structural shift beneath the surface. While overall capital flows remain robust, the composition of investment has changed materially. Understanding these shifts requires looking beyond aggregate data and examining the mechanisms through which capital is actually deployed.

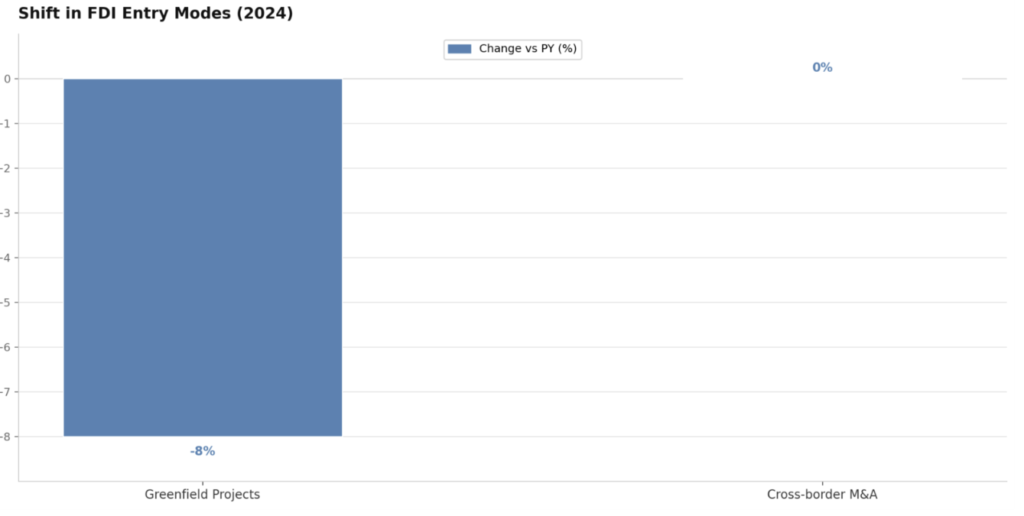

Chart 1: UN Trade and Development

In 2024, greenfield investment projects declined by roughly 8% globally, while cross-border mergers and acquisitions (M&A) remained comparatively stable in value. This divergence reflects growing investor caution toward projects exposed to long development timelines, regulatory approvals, land acquisition, and construction risk. Rather than avoiding emerging markets outright, investors are increasingly choosing entry modes that limit execution exposure.

Chart 2: ASEAN Total FDI Inflows (USD Billion), 2019–2024. Source: UNCTAD

Despite a sharp contraction in 2020 driven by the pandemic, ASEAN inflows recovered rapidly, reaching approximately US$235 billion in 2024. Notably, this post-pandemic recovery was not simply a return to pre-2020 norms. The jump from US$175 billion in 2021 to US$223 billion in 2022 reflects a structural step-up driven by supply chain diversification, nearshoring, and growing confidence in ASEAN as a manufacturing hub. The continued plateau near US$230–235 billion in 2023–2024 signals a new floor for regional investment volumes. For investors and policymakers alike, this sustained demand underscores why improving execution frameworks has become the key variable in attracting long-term capital.

Why Traditional Risk Frameworks Are Evolving

Country risk metrics—such as sovereign credit ratings and political stability indices—often fail to capture the risks that truly dominate investment outcomes today. Execution risk manifests at the project level. It encompasses delays in permitting, land clearance challenges, contractual enforcement issues, payment discipline, and the ability of local counterparties to deliver complex projects on time and within budget.

In Vietnam, for example, multiple infrastructure and energy projects have experienced significant delays due to administrative bottlenecks rather than funding constraints. Industry studies consistently identify site clearance and multi-agency coordination as persistent hurdles. These are risks that are difficult to diversify at the portfolio level and are often inadequately priced during initial investment decisions.

Capital Structure Adjustments: How Investors Are Responding

The growing prominence of execution risk has driven a notable shift in investment structures. Rather than establishing new operations from scratch, foreign investors increasingly favor; Acquiring stakes in operating businesses, investing in brownfield or platform assets, and partnering with established local operators.

In Vietnam, foreign participation in sectors such as ports, logistics, healthcare, and industrial real estate has increasingly occurred through M&A rather than greenfield entry. By entering through existing platforms, investors gain immediate access to operating cash flows, established regulatory approvals, and local management capabilities—reducing exposure to execution uncertainty without abandoning growth opportunities.

Execution Risk in Practice: Policy Ambition vs Delivery Capacity

The gap between policy intent and project execution is particularly visible in Southeast Asia’s infrastructure and energy markets. Governments have announced ambitious transition targets, yet project pipelines frequently stall due to contractual disputes or administrative delays, not a lack of capital.

In Vietnam’s renewable energy sector, developers behind more than 170 solar and wind projects have reported delayed or partial payments under existing power purchase agreements. This has prompted some investors to pause reinvestment despite strong long-term market fundamentals. These experiences reinforce the investor focus on counterparty reliability and contractual enforcement.

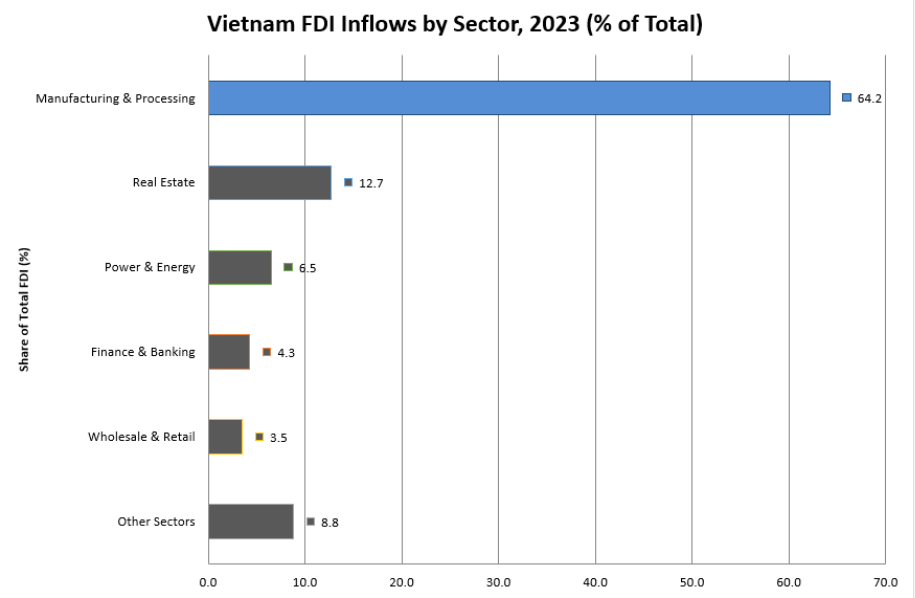

Chart 3: Vietnam FDI Inflows by Sector, 2023 (% of Total) (Source: Ministry of Planning & Investment Vietnam)

Sectoral allocation provides a practical lens for observing execution risk. Manufacturing and processing dominates Vietnam’s inbound FDI at 64.2%—a deliberate preference for sectors where execution pathways are well-established and supply chains are mature. In contrast, sectors like power and energy (6.5%) and finance (4.3%) attract smaller shares. This is not due to a lack of underlying opportunity, but because execution complexity remains high. Investors continue to commit capital, but strictly in sectors where they can reliably convert investment into returns.

Despite heightened execution risk, emerging markets remain central to global capital deployment. Unlike advanced economies—where much investment involves replacing aging infrastructure—many emerging Asian economies are still expanding core infrastructure capacity, creating sustained long-term demand for capital across energy, transport, logistics, digital infrastructure, and urban development. From a capital allocation perspective, this distinction is critical: while developed markets typically offer lower execution risk, they also present fewer opportunities for large-scale capacity expansion. Emerging markets, by contrast, combine higher complexity with structurally stronger long-term growth in asset demand. As a result, the challenge for investors is not whether to allocate capital to emerging markets, but how to structure that exposure to manage execution risk effectively.

Investment Implications for Global Capital Markets

Execution risk introduces severe constraints for international investors. Rapidly evolving regulatory frameworks, currency mismatches, and a reliance on complex blended financing (combining domestic banks, multilateral lenders, and institutional capital) all extend development timelines.

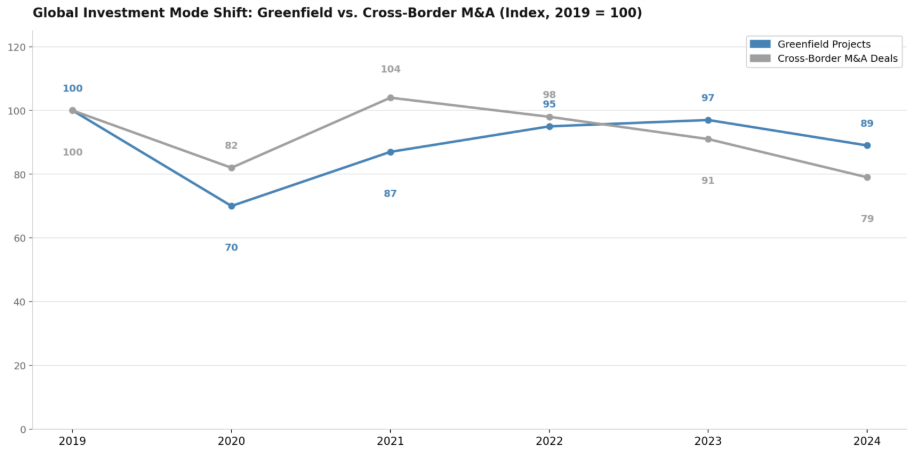

Chart 4: Global Investment Mode Shift – Greenfield vs. Cross-Border M&A (Index, 2019 = 100). Source: UNCTAD

This structural shift is most clearly observed in the widening gap between greenfield activity and M&A over the past five years. Following the 2020 pandemic dip, cross-border M&A rebounded strongly. Greenfield investment, however, recovered much more slowly, ending 2024 approximately 11% below its 2019 baseline.

This gap is not cyclical noise; it is a deliberate rotation away from new-build project risk. For policymakers relying on greenfield investments to expand infrastructure, this trend is a stark warning. To attract long-term capital at scale, governments must focus not just on announcing new projects, but on building administrative and contractual credibility.

Long‑Term Opportunities at the Edge of Certainty

Emerging Asia remains one of the most vital arenas for long-term capital. Institutional investors, including pension funds and infrastructure managers—continue to seek assets capable of generating stable, long-duration returns. As execution frameworks incrementally improve and local operating platforms mature, the opportunities to deploy capital with certainty will expand.

Key Takeaways

Capital allocation to emerging Asia is undergoing a structural shift. While country risk remains relevant, execution risk has become the dominant variable shaping investment decisions. Investors are no longer asking only whether a country is investable, but whether capital can be reliably deployed, operated, and repatriated within complex local systems. This shift does not signal a retreat from emerging markets. Instead, it reflects a more disciplined, selective approach to capital deployment—one that prioritizes execution capability, governance, and structural resilience over headline growth narratives. For policymakers, improving administrative efficiency and project delivery capacity is increasingly critical to attracting long‑term capital. For investors, the opportunity lies in navigating the edge of certainty—where execution risk is understood, structured, and priced rather than avoided.

For deeper insights on capital markets, infrastructure investment, and emerging market dynamics, follow Dealflow for research‑driven perspectives via LinkedIn or explore further analysis at Dealflow.sg.