Vietnam’s economic ascent has been powered by export-led manufacturing, FDI inflows, and rapid urbanization. Between 2010 and 2019, GDP growth averaged approximately 6–7% annually, placing Vietnam among the fastest-growing economies in Asia. Manufacturing now accounts for roughly one-quarter of GDP, while industrial activity consumes nearly half of national electricity output. Yet infrastructure development has not expanded at the same pace.

The Scale of the Infrastructure Financing Gap

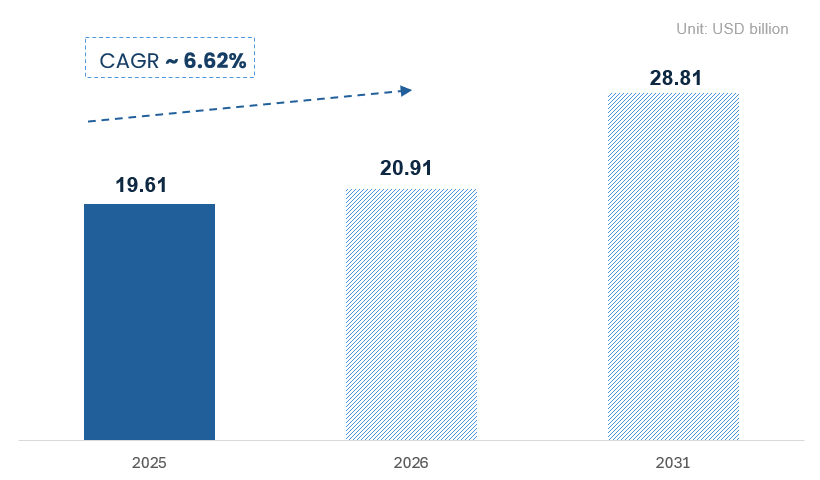

According to regional development bank estimates, Vietnam requires approximately USD 25–30 billion annually in infrastructure investment through 2030. This includes transportation networks, industrial utilities, renewable energy capacity, water treatment systems, and urban resilience infrastructure.

Vietnam Infrastructure Market Size Projection (2025–2031)

Public capital expenditure and state-owned enterprise funding alone cannot meet this requirement. Domestic banks, while active in project lending, face balance sheet constraints and regulatory capital limits that restrict long-tenor infrastructure exposure.

The result is a structural financing gap — not merely a shortage of funds, but a shortage of patient, risk-calibrated capital aligned with long-term sustainability objectives.

Climate Commitments as a Financial Variable

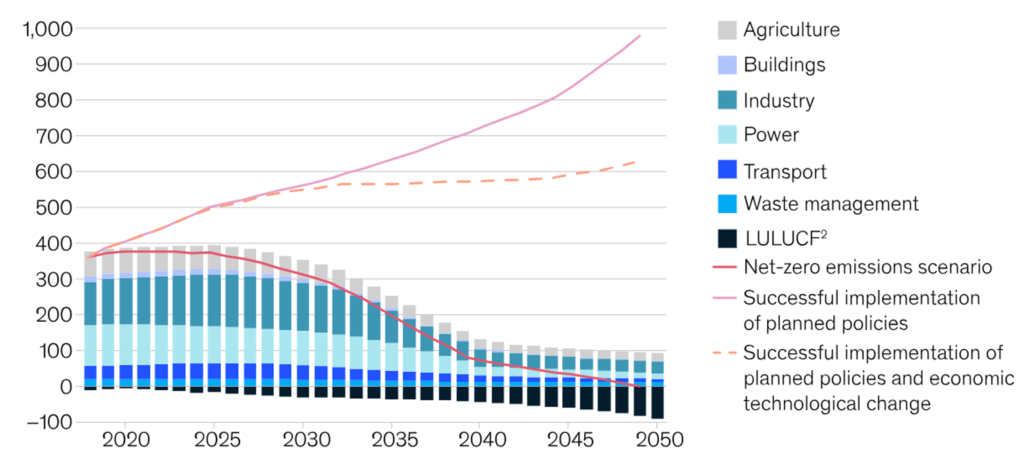

Vietnam’s commitment to achieve net-zero emissions by 2050 fundamentally changes infrastructure economics. Projects must now account for carbon intensity, transition risk, and regulatory tightening.

Vietnam’s Net-Zero Emissions Pathway to 2050

Infrastructure is no longer judged solely by IRR or construction cost. It is evaluated against lifecycle emissions, energy efficiency, and resilience against climate shocks. Coastal cities such as Da Nang face heightened scrutiny because physical climate risks directly affect asset durability and insurance costs.

Why Da Nang Is Strategically Important

Da Nang occupies a critical economic position in Central Vietnam. It serves as a port gateway, logistics hub, and industrial node connected to the East–West Economic Corridor. It also markets itself as a smart and technology-forward city.

However, it is also one of the most climate-exposed urban centers in the country due to flooding and storm risk. This dual reality makes Da Nang an ideal test case for sustainable infrastructure finance: high growth potential combined with high environmental exposure.

IFC’s Expanding Climate Finance Role in Vietnam

The International Finance Corporation (IFC), has emerged as a central player in Vietnam’s sustainable finance landscape. With a committed portfolio exceeding USD 2 billion in the country, IFC has steadily expanded its exposure to renewable energy, green buildings, sustainable transport, and climate-resilient infrastructure. Vietnam’s rapid urbanization and industrialization—combined with its vulnerability to climate change—have made it a priority market within IFC’s regional strategy.

This expansion aligns with IFC’s global pivot toward climate finance. More than one-third of IFC’s long-term commitments worldwide are now climate-aligned, reflecting a structural shift in development finance toward decarbonization and resilience. In Asia, this has translated into increased support for solar and wind power projects, energy efficiency financing, and sustainable urban development platforms.

In Vietnam specifically, IFC’s climate investments also aim to catalyze private capital mobilization. By anchoring transactions and applying international environmental and governance standards, IFC not only deploys its own capital but also reduces barriers for commercial banks and institutional investors to participate in green financing structures. Over time, this deepens Vietnam’s sustainable capital markets and strengthens the pipeline for climate-resilient infrastructure development.

IFC as a Risk Recalibration Mechanism

Infrastructure in emerging markets is typically priced with a structural risk premium. Equity return expectations often range from 14–18%, compared to 8–12% in developed markets. Long-term project finance debt can carry spreads that are 200–300 basis points higher. Much of this differential reflects perceived risks—regulatory shifts, governance variability, and execution uncertainty—rather than purely unstable cash flows.

The International Finance Corporation (IFC), a member of the World Bank Group, helps narrow this gap through institutional discipline.

First, IFC applies rigorous multi-layered due diligence. Technical feasibility, sponsor credibility, legal enforceability, and financial resilience are assessed before capital deployment. Transactions involving multilateral participation have been observed to reduce financing costs by 50–150 basis points. For a USD 150 million project, a 100-basis-point reduction can save roughly USD 1.5 million annually in interest expense.

Second, IFC enforces internationally recognized Environmental and Social Performance Standards. Globally, infrastructure projects facing ESG disputes have recorded cost overruns exceeding 20% and delays of 12–24 months. Structured stakeholder engagement, environmental safeguards, and transparent reporting significantly reduce these downside risks.

Third, IFC maintains continuous monitoring throughout the project lifecycle. Regular reporting, compliance checks, and governance oversight limit post-investment drift—one of the core concerns in emerging markets.

Taken together, IFC’s participation acts as a powerful signaling mechanism. It communicates to global investors that a project meets international governance and ESG benchmarks. This strengthens investor confidence, broadens institutional participation, and gradually compresses the perceived risk premium attached to emerging market infrastructure.

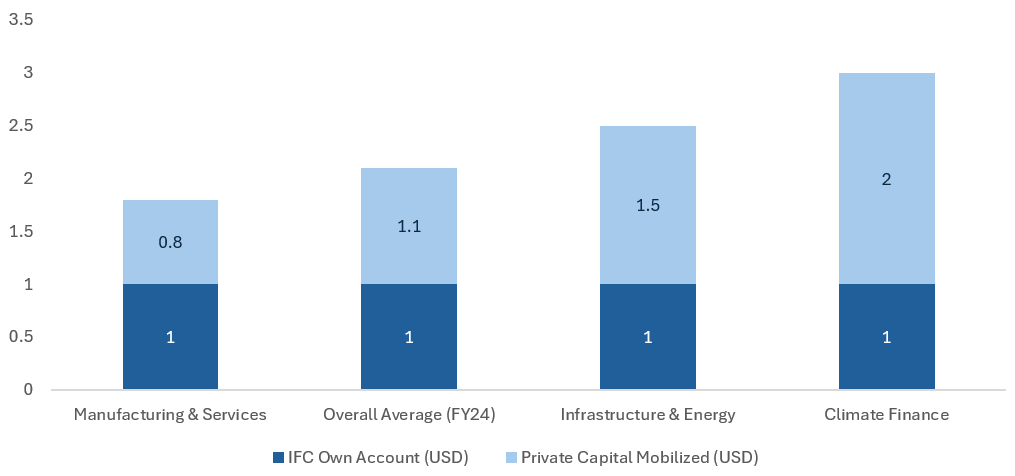

The Capital Mobilization Multiplier

One of IFC’s most significant contributions extends beyond its own balance sheet: its ability to mobilize private co-investment at scale. Historically, for every USD 1 of IFC capital deployed, an additional USD 1–2 has been mobilized from private investors, depending on sector, risk profile, and transaction structure. In certain infrastructure and climate-focused projects, the mobilization ratio can be even higher when blended finance or parallel lending structures are applied.

This multiplier effect is particularly critical in Vietnam’s infrastructure sector, where long-term capital requirements far exceed the fiscal capacity of public budgets. As urbanization accelerates and energy transition targets tighten, financing gaps in transport, renewable power, water treatment, and climate-resilient urban systems continue to widen. Development finance institutions like IFC therefore play a catalytic role in bridging this gap by crowding in commercial banks, export credit agencies, and institutional investors.

IFC’s Mobilization Multiplier: Scaling Private Capital for Vietnam’s Green Transition.

In the context of Da Nang, IFC-backed green infrastructure projects serve as powerful investability signals. Their structured governance, ESG compliance, and risk mitigation frameworks reduce uncertainty for international lenders and infrastructure funds. As a result, projects anchored by IFC are more likely to attract diversified capital pools, accelerating financial close and strengthening long-term capital formation in Vietnam’s sustainable infrastructure market.

Institutionalization of Infrastructure Assets

Beyond capital provision, IFC contributes to institutionalizing infrastructure as an asset class. Projects structured Beyond capital provision, the International Finance Corporation (IFC), a member of the World Bank Group, plays a structural role in institutionalizing infrastructure as a recognized asset class in emerging markets. Projects developed under IFC frameworks typically adopt enhanced financial transparency, standardized governance reporting, environmental monitoring systems, and formal stakeholder engagement mechanisms. These institutional layers reduce information asymmetry and align projects with global reporting norms.

This standardization has measurable capital market implications. Globally, the green bond market has surpassed USD 2 trillion in cumulative issuance, while sustainability-linked financing continues to expand across Asia. Infrastructure projects that meet robust ESG and disclosure benchmarks are more likely to qualify for green bonds or sustainability-linked loans, often benefiting from pricing advantages of 25–75 basis points compared to conventional financing.

Over time, institutional structuring reduces transaction friction. Refinancing options expand, secondary market participation increases, and long-term investors—such as pension funds and insurance companies—become more willing to allocate capital. As transparency improves and governance becomes predictable, infrastructure gradually transitions from a high-risk frontier exposure to a scalable institutional asset class.

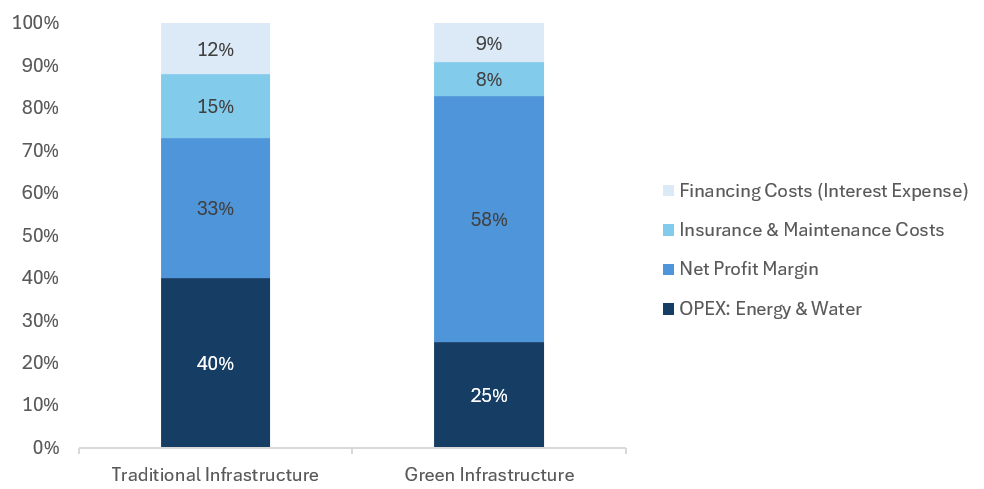

Green Infrastructure as Financial Risk Management

Green infrastructure is often discussed in environmental terms. However, its financial logic is equally compelling. Infrastructure assets operate over multi-decade horizons. Decisions made during the design and structuring phase determine operational performance, regulatory compliance, and exposure to climate volatility.

Green Infrastructure: Strategic Risk Mitigation and Margin Expansion

Lifecycle Efficiency and Operating Margin Stability

Embedding renewable energy integration, energy-efficient building design, and advanced wastewater treatment reduces operating costs over time. Energy efficiency directly improves margin stability in industrial parks. Water recycling systems lower input cost exposure. Smart grid integration reduces downtime risk. These operational efficiencies translate into stronger debt service coverage ratios and improved credit metrics.

Access to Green Capital Pools

Sustainability-linked loans and green bond issuance volumes in Asia have expanded dramatically over the past decade, reaching tens of billions of dollars annually. Projects aligned with recognized environmental standards are better positioned to access these capital pools at competitive spreads. Lower cost of capital enhances project viability and increases net present value over long asset lifecycles.

Climate Resilience as Asset Protection

Coastal cities face rising flood and storm intensity. Infrastructure built without adaptive engineering risks significant impairment over time. Climate-resilient design — including improved drainage systems, elevated structural standards, and energy redundancy — reduces insurance exposure and long-term repair costs. For investors applying climate stress testing frameworks, resilient assets carry lower downside volatility.

Industrial Competitiveness in a Low-Carbon Supply Chain Era

Vietnam’s manufacturing sector accounts for approximately 45–50% of national electricity consumption. As multinational corporations face decarbonization mandates, supply chain emissions have become a key procurement criterion.

Renewable Energy Integration Within Industrial Parks

Vietnam’s renewable energy share has increased significantly in recent years, particularly solar and wind capacity. However, coal remains a dominant generation source. Industrial parks capable of integrating renewable energy solutions offer tenants the ability to reduce Scope 2 emissions. This becomes a competitive advantage when courting multinational manufacturers.

ESG-Driven Tenant Selection

Institutional investors increasingly evaluate tenant ESG profiles within infrastructure portfolios. Industrial zones hosting high-emission tenants may face reputational and transition risks. Green industrial infrastructure improves tenant quality, enhances long-term lease stability, and supports valuation resilience.

Long-Term Asset Liquidity

As ESG integration deepens in global capital markets — with over USD 30 trillion managed under ESG mandates — infrastructure assets aligned with decarbonization pathways benefit from stronger secondary market liquidity. IFC-backed projects in Da Nang thus sit at the intersection of industrial competitiveness and global capital alignment.

Conclusion: Da Nang as a Prototype for Institutional Sustainable Capital

IFC’s involvement in green urban and industrial infrastructure in Da Nang reflects more than project-level financing. It represents a structural shift in Vietnam’s infrastructure capital formation model.

Risk recalibration, sustainability integration, and private capital mobilization are transforming infrastructure into a disciplined institutional asset class.

Da Nang functions as a prototype. If sustainable infrastructure finance can succeed in a high-growth, climate-exposed secondary city, the model can be replicated across Vietnam.

The next phase of Vietnam’s development will not be defined solely by GDP expansion. It will be defined by the resilience, governance quality, and sustainability alignment of its infrastructure base. Sustainable capital is no longer optional. It is becoming foundational.

To explore active opportunities or discuss your Vietnam infrastructure thesis, connect with DealFlow.sg or follow our latest insights on LinkedIn.