From Digital Infrastructure to Institutional Capital

Vietnam’s economic ascent has historically been powered by export manufacturing, labor arbitrage, and foreign direct investment. Yet as the country advances into its next development phase, the sources of durable growth are shifting. Increasingly, value creation is determined not by production volume, but by control over digital infrastructure, data flows, and compute capacity.

At the center of this transition lies an asset class that until recently sat at the margins of macroeconomic analysis: data centers. Once treated as a technical utility, data centers are now emerging as strategic infrastructure—absorbing institutional capital, shaping energy demand, and anchoring digital sovereignty. In Vietnam, this evolution is occurring at scale, driven by structural demand rather than speculative cycles.

A Market Scaling Rapidly — by Regional Standards

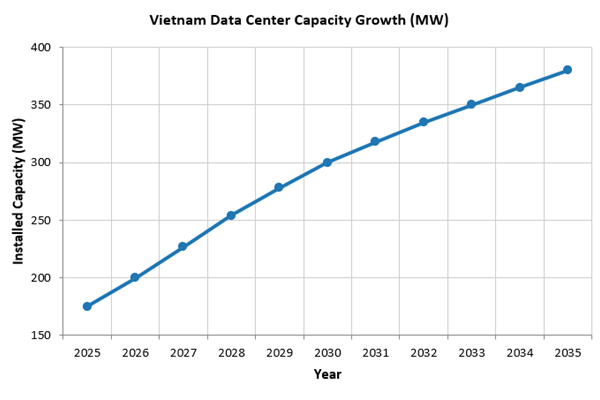

Figure 1: Projected Vietnam Data Center Installed Capacity Growth (2025–2035)

Looking at the graph above, Vietnam’s data center market is one of the fastest‑growing in Southeast Asia, though from a low base. Installed capacity reached approximately 175 MW in 2025, and is projected to more than double to 360–400 MW by the early 2030s, implying a high‑single‑ to low‑double‑digit CAGR over the next decade. In value terms, estimates place the market at USD 1.2–1.4 billion in 2025, with projections ranging between USD 2.5–4.0 billion by 2032, depending on hyperscale deployment and AI workload adoption.

This growth is driven by three structural factors: Vietnam’s digital economy is expanding at roughly 20% annually and contributes over 18% of GDP as of 2024; enterprise cloud adoption is increasing across key sectors such as finance, manufacturing, and government; and regulatory pressures are favoring domestic data storage and processing. As a result, the demand curve is reinforced by policy rather than driven by cyclical forces.

Data Localization as an Infrastructure Catalyst

Vietnam’s evolving data governance framework has materially altered the economics of compute infrastructure. The Personal Data Protection Decree and the subsequent Law on Data, effective from 2025 to 2026, significantly tighten requirements on cross-border data transfers, with non-compliance penalties tied to revenue.

For enterprises operating in banking and payments, e-commerce and logistics, telecommunications, and government and public services, maintaining local compute capacity is no longer optional. This has shifted demand away from offshore hosting toward onshore, enterprise‑grade facilities, accelerating absorption rates in Tier III and Tier IV data centers—segments projected to grow faster than the market average.

Capital Intensity and the Infrastructure Profile

Unlike traditional technology investments, data centers exhibit characteristics more akin to core infrastructure: they require high upfront capital expenditure, have long asset lives of 20–30 years, and generate stable, contract-driven cash flows once stabilized. In Vietnam, construction costs average USD 6–8 million per MW, which is significantly lower than in markets such as Singapore, Japan, or South Korea, where costs often exceed USD 10–15 million per MW.

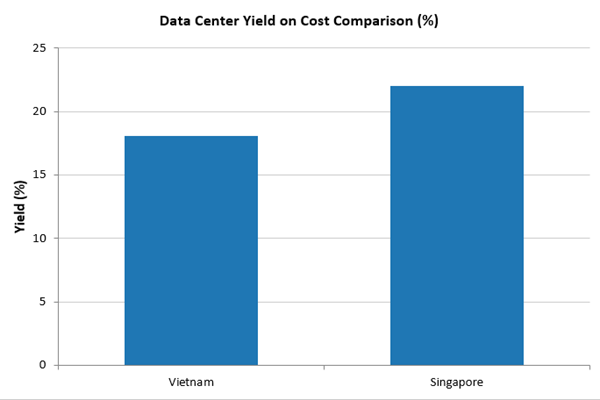

Figure 2: Data Center Yield on Cost Comparison Between Vietnam and Singapore (%)

This distinct cost advantage has positioned Vietnam as the second-most lucrative market in Southeast Asia for data center investment returns, boasting estimated yields on cost of 17–19%. In comparison, mature markets typically generate returns in the low-teens. For institutional investors, this frames Vietnamese data centers as a premier hybrid asset class—marrying the defensiveness of core infrastructure with the high-growth upside of an emerging market.

Energy Is the Binding Constraint

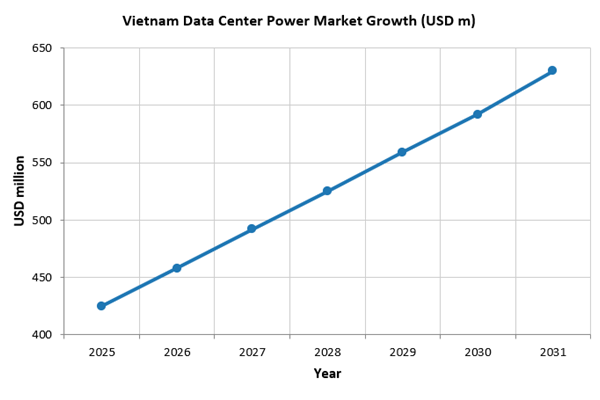

Figure 3: Projected Growth of Vietnam’s Data Center Power Market (2025–2031, USD Million)

Data centers remain among the most energyintensive assets in the modern economy. Vietnam’s datacenter power market alone was valued at approximately USD 400–425 million in 2025, projected to grow at 6–7% annually through the early 2030s.

Simultaneously, rack densities are surging toward 30–40 kW per cabinet in AI-optimized facilities. Coupled with increasingly stringent power reliability requirements and grid pricing volatility, energy has become a material underwriting factor. These dynamics have thrust data centers into the center of the energy transition conversation, accelerating institutional interest in renewable power purchase agreements (PPAs), co-location with solar and wind assets, and advanced cooling systems. The convergence of green finance and digital infrastructure is no longer theoretical—it is a baseline requirement for project feasibility.

The Structural Evolution of Vietnam’s Data Center Market

The strategic shift underway is not merely quantitative but fundamentally structural. Early-stage data center development in Vietnam was largely focused on smaller, enterprise-oriented facilities designed to meet localized or single-tenant demand.

In contrast, the current development pipeline is increasingly dominated by hyperscale campuses exceeding 100 MW, purpose-built AI-optimized designs, and platform-level developments that integrate multiple phases and capabilities rather than standalone assets. By late 2025, Vietnam’s announced and under-construction data center pipeline had surpassed 500 MW, signaling a clear transition from opportunistic, project-by-project development to coordinated, national-scale infrastructure planning. This evolution reflects not only rising demand but also a maturation of the investment landscape, where scale, standardization, and long-term strategic positioning are becoming central.

Adopting a platform-based approach enhances capital efficiency by enabling phased expansion, shared infrastructure, and better utilization of power and land resources. It also strengthens regulatory compliance, as larger, more structured developments are better equipped to meet increasingly stringent data localization, security, and energy requirements. At the same time, these platforms are more attractive to global co-investors—such as institutional funds and hyperscale cloud providers—who prioritize scalability, reliability, and alignment with international standards.

Implications for Capital Allocation

For investors, Vietnam’s data center sector is no longer a short-term trade but a long-duration, infrastructure-style allocation. Returns are increasingly shaped by duration rather than velocity, policy alignment rather than regulatory or pricing arbitrage, and energy security rather than pure occupancy metrics. This reflects a shift toward more stable, contract-backed income streams where long-term positioning and operational resilience matter more than rapid leasing cycles.

As a result, the asset class naturally attracts infrastructure funds, sovereign and quasi-sovereign capital, and long-duration private credit providers, all of whom are aligned with extended investment horizons and predictable cash flows. At the same time, as Vietnam’s domestic capital markets continue to deepen, data centers present a compelling pathway for local institutional investors—such as pension funds and insurance companies—to participate. In doing so, they enable the recycling of national savings into productive, technology-enabling assets that support broader economic modernization.

Key Takeaways

Vietnam’s growth is entering a more capital-intensive phase, where control over compute capacity is becoming a key driver of competitiveness. At the intersection of digital sovereignty, energy policy, and institutional capital, data centers are no longer peripheral real estate—they are core economic infrastructure. Countries that successfully institutionalize compute will define the next decade of growth, and Vietnam is positioning itself among them.

For deeper insights on capital markets, infrastructure investment, and emerging market opportunities, follow Dealflow for research-driven perspectives on global finance via LinkedIn or explore further analysis at Dealflow.sg.