Over the past decade, China has quietly constructed one of the most comprehensive green finance architectures anywhere in the world. While global conversations on sustainable finance tend to spotlight regulatory advances in Europe or institutional capital flows in the United States, China has developed a parallel system that operates at a scale few other economies can match. From green credit markets to sovereign green bonds and carefully designed regional pilot zones, the country has woven sustainability objectives directly into the fabric of its financial system. This integration is not merely environmental; it forms part of a deliberate economic strategy to channel capital toward industrial transformation and long-term environmental resilience.

Given China’s position as the world’s largest energy consumer and a leading carbon emitter, the outcomes of this green finance experiment carry profound global significance. For investors and capital allocators, the model offers a powerful case study in how large-scale policy coordination can accelerate the deployment of sustainable capital while simultaneously supporting economic upgrading. China is no longer just an emerging market participant in green finance — it has become one of the most important real-world laboratories for testing how green capital can be mobilized at national scale.

The Rise of China’s Green Credit System

China’s green finance model stands out because of the central role played by the banking sector. In contrast to many Western markets where capital markets and institutional investors lead sustainable financing, China’s system remains overwhelmingly bank-centric. As a result, green lending by commercial banks has emerged as the primary engine of the country’s climate finance strategy.

Explosive Growth in Outstanding Green Credit Balances

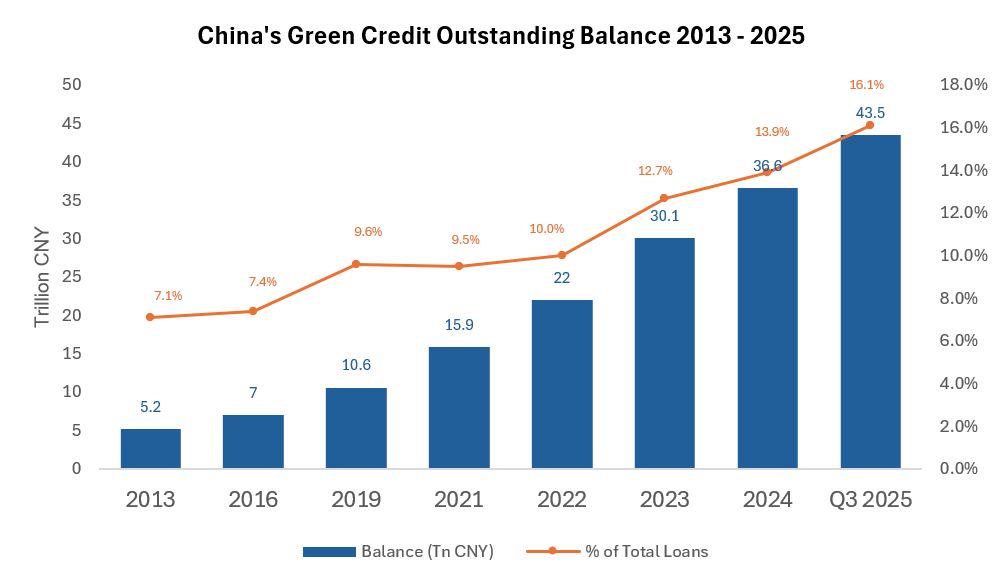

As the accompanying chart illustrates, outstanding green credit balances have grown dramatically over the past twelve years, rising from approximately CNY 5.2 trillion in 2013 to CNY 43.5 trillion by the third quarter of 2025. At the same time, the share of green credit within total bank lending has climbed steadily from 7.1 percent to 16.1 percent. This is not organic market evolution but the outcome of sustained, high-level policy direction from the People’s Bank of China and other regulators.

Source: PBOC; Green Finance & Development Center

This rapid expansion has been achieved through a combination of regulatory incentives and strategic coordination across state-owned banks, creating a robust foundation for China’s climate finance ambitions and giving investors a clear trajectory of continued scale-up.

Policy Mechanisms Driving Expansion and Strong Asset Quality

The policy toolkit — including preferential capital weighting for green loans, dedicated green finance guidelines for commercial banks, and mandatory environmental risk disclosure frameworks — has successfully embedded sustainability criteria into everyday credit decisions. These measures have created a predictable and scalable financing environment that encourages banks to prioritize renewable energy, electric vehicles, and low-carbon infrastructure without sacrificing commercial returns. For institutional investors monitoring Chinese financial institutions or green asset exposure, this policy consistency translates into greater visibility and reduced execution risk.

Equally significant is the strong performance of the green credit portfolio itself. The non-performing loan ratio for green loans has remained consistently and materially lower than the broader banking sector average, underscoring that policy-directed lending can align with prudent risk management. This track record gives investors confidence that large-scale green finance deployment in China is not only environmentally effective but also financially resilient, opening attractive avenues for participation through bank lending platforms, green bonds, and project-level debt.

Green Finance as a Strategic Industrial Policy Tool

For decades, China’s economic rise was powered by steel, cement, coal, and heavy manufacturing — sectors that delivered rapid growth but also locked in substantial environmental liabilities. Green finance now serves as the financial bridge out of that legacy model, systematically redirecting capital away from high-carbon activities toward cleaner alternatives. This reallocation is deliberate and structural, not merely incremental.

Through targeted incentives, banks are channeling funds into renewable energy infrastructure, electric vehicle supply chains, advanced battery manufacturing, energy storage solutions, and green urban development. These sectors represent the next wave of Chinese industrial competitiveness — higher-value, technology-driven, and export-oriented. The policy framework effectively turns sustainability objectives into a competitive advantage, creating multi-year investment pipelines that investors can underwrite with confidence.

In this context, green finance functions as dual-purpose capital: it delivers measurable environmental outcomes while simultaneously accelerating China’s transition toward a high-tech, services-led economy. For buyers of green assets and infrastructure funds, this duality means exposure to projects that enjoy both strong policy tailwinds and genuine market demand, while mitigating stranded-asset risk in legacy carbon-intensive industries.

Regional Pilot Zones: Testing Grounds for Innovation

Recognizing the need for practical experimentation before nationwide rollout, the central government launched the first Green Finance Reform and Innovation Pilot Zones in 2017 across provinces including Zhejiang, Jiangxi, Guangdong, Guizhou, and Xinjiang. These zones were explicitly designed as controlled laboratories to test regulatory innovations, financial instruments, and disclosure standards under real-market conditions.

Within the pilots, authorities introduced specialized green credit evaluation systems, environmental information disclosure platforms, green bond issuance programs, and performance-based fiscal incentives for low-carbon projects. The localized flexibility allowed regulators to observe what works — and what does not — without risking systemic disruption.

The outcomes have been impressive: between 2018 and 2021, green credit growth in pilot zones averaged approximately 21 percent annually, well above the national average. In Huzhou, for instance, green credit exceeded 22 percent of total loans by 2022. These demonstrated successes have provided the evidence base for scaling successful mechanisms nationwide, giving investors a clear signal that once a policy is validated regionally, it tends to be replicated at national level with high predictability.

Supporting the Transition of Resource-Dependent Cities

Many Chinese cities were built around extractive industries — coal mining, oil production, and metal processing — that once formed the backbone of regional economies. Resource depletion and the national pivot to cleaner energy have now left numerous localities facing structural decline, creating both social and economic challenges that require targeted financial solutions.

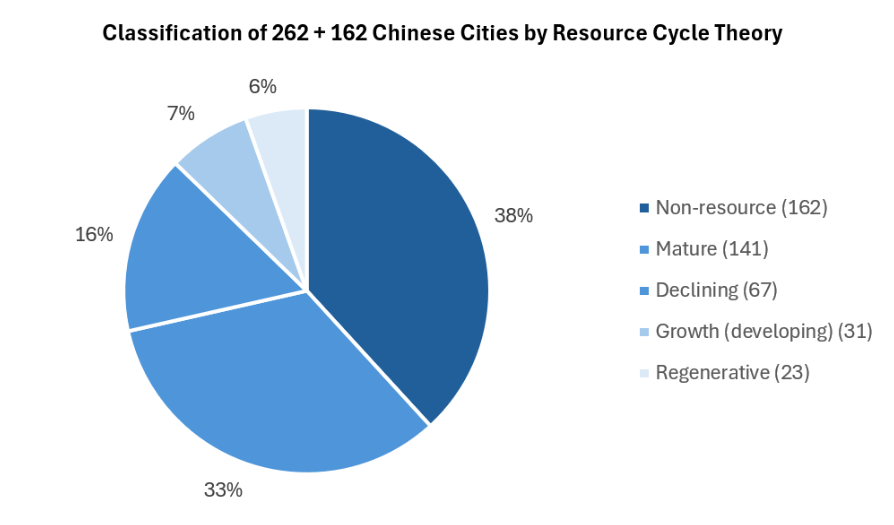

Recent analysis applying Resource Cycle Theory to 424 Chinese cities (162 non-resource and 262 resource-dependent) offers a precise diagnostic. As the accompanying pie chart shows, 38 percent of cities are non-resource based, while among resource cities 33 percent remain in the mature stage of heavy dependence, 16 percent are already classified as declining, and only 6 percent have reached the regenerative stage where diversification has taken hold. This distribution highlights the scale of the transition challenge still ahead.

Source: Wang & Gao (2024), Nature HSSC; State Council (2013).

Green finance is now being deployed precisely to accelerate diversification in these regions — financing renewable energy projects, environmental remediation, and new industrial clusters that can replace lost extractive jobs and output. The approach demonstrates how financial policy can address not only climate goals but also regional equity and stability imperatives, creating fresh investment opportunities in transition-themed infrastructure that would otherwise remain underserved.

Global Implications and Comparative Advantages

China’s green finance architecture differs fundamentally from Western approaches: it leverages the dominant role of state-owned banks and top-down policy coordination rather than relying primarily on private capital markets and voluntary investor pressure. This structure enables the rapid mobilization of truly massive capital volumes in alignment with national priorities.

Because of its scale and proven execution speed, elements of the Chinese model — standardized green credit guidelines, integrated environmental risk assessments, and incentive-driven frameworks — are increasingly studied by policymakers in other emerging economies. For global investors, this means China’s experience can serve as a blueprint for how large-scale sustainable finance can be implemented in bank-centric systems where private markets are still maturing.

As worldwide climate investment needs continue to expand, the Chinese experiment is reshaping expectations about the speed and scale at which green capital can be deployed. Even modest shifts in lending patterns within China’s financial system redirect hundreds of billions in funding, creating ripple effects across global supply chains and capital allocation decisions.

Key Takeaways

China’s green finance experiment demonstrates how an emerging economy can harness a bank-centric system to channel capital toward sustainability at a truly national scale. With green credit outstanding reaching CNY 43.5 trillion and comprising 16.1 percent of total loans by Q3 2025, alongside targeted regional pilots and resource-city diversification programs, the framework blends environmental imperatives with industrial upgrading objectives in a uniquely effective manner.

For policymakers, the emphasis must remain on refining disclosure standards and regulatory consistency to unlock additional international capital inflows. For investors and buyers, the opportunity lies in engaging with one of the largest and most rapidly evolving sustainable finance ecosystems in the world — spanning renewable infrastructure, green credit portfolios, and transition initiatives across hundreds of cities. As policy-driven capital allocation deepens and market mechanisms mature, the convergence of green finance and China’s industrial transformation will continue to shape global capital flows for years to come.

For deeper insights on capital markets, infrastructure investment, and emerging market opportunities, follow Dealflow for research-driven perspectives on global finance via LinkedIn or explore further analysis at Dealflow.sg.