Driven by restrictive monetary policies, a wave of distressed M&A is accelerating in Vietnam. Foreign Private Equity (PE) funds are currently executing a systemic, quiet accumulation of industrial assets, seizing a once-in-a-decade opportunity to acquire fragmented manufacturing and packaging facilities at deep valuation discounts.

Why are Distressed Assets Booming in Vietnam?

The proliferation of distressed M&A in Vietnam is the direct result of compounding macroeconomic pressures. Severe internal financial strain and the rapidly depleting endurance of domestic firms have jointly created an unprecedented accumulation opportunity, driving foreign capital directly into highly vulnerable industrial sectors.

Internal Financial Pressure: The Credit Crunch and Export Volatility

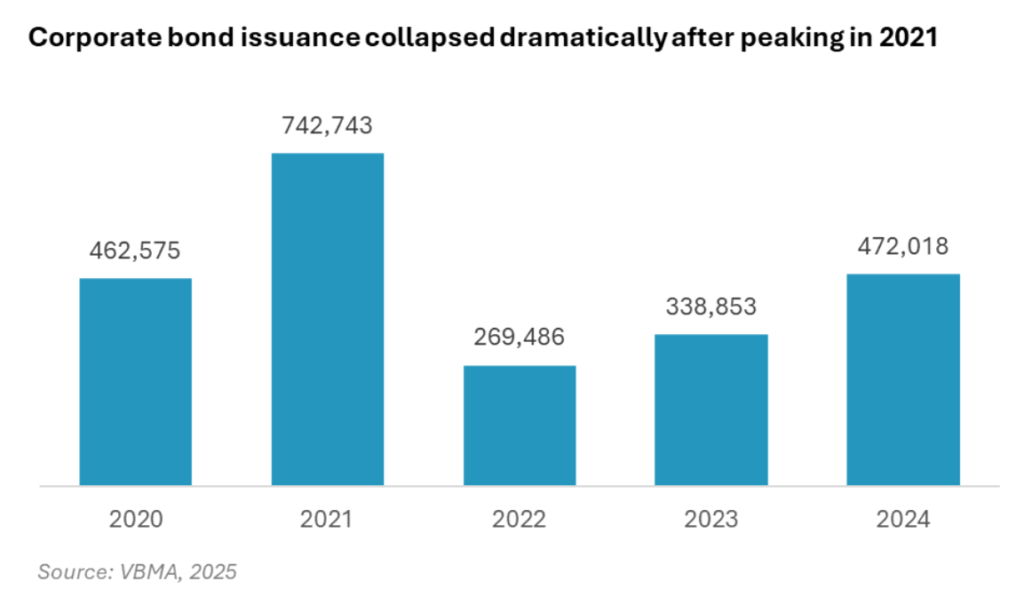

Figure 1: Corporate bond issuing value (Billion VND)

The current distressed asset environment is primarily driven by a dual macroeconomic shock: a severe domestic credit crunch coupled with a collapse in global export revenues. Between 2023 and 2025, aggressive US Federal Reserve rate hikes forced the State Bank of Vietnam to tighten liquidity to defend the Dong, driving corporate lending rates to levels that effectively priced SMEs out of the debt market.

This banking contraction was exacerbated by a systemic collapse in the domestic corporate bond market—which plummeted from 742,743 billion VND in 2021 to 338,853 billion VND in 2023 following regulatory crackdowns—leaving highly leveraged firms stranded without refinancing options. Simultaneously, prolonged inventory destocking by US and EU retailers triggered a sharp drop in new export orders, severing crucial operational cash flows. Ultimately, this fatal combination of soaring capital costs and decimated top-line revenues rapidly exhausted the financial endurance of domestic industrial firms.

Depleted Endurance of Domestic Firms and Rising NPLs

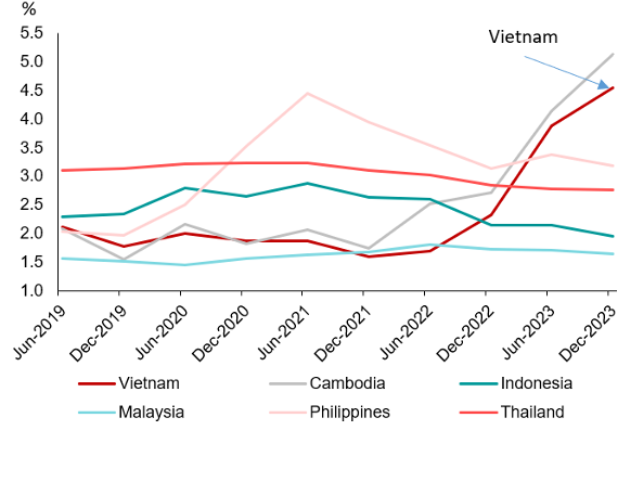

Figure 2: NPL Ratio by Country (%)

Highly leveraged Vietnamese SMEs, once reliant on rolling over short-term debt, have collapsed under recent liquidity constraints. Consequently, bad debts in Vietnam increased steadily throughout 2022 and 2023, surging to levels significantly higher than in many other ASEAN countries. This acute financial distress culminated at the end of July 2024, when the system-wide non-performing loan (NPL) ratio reached 4.8%, decisively breaching the State Bank’s 3% safety threshold.

The direct effect of this mounting bad debt is a paralyzed domestic lending market that has stranded SMEs with a massive USD 24 billion credit gap. Cut off from refinancing and lacking formal Chapter 11-style bankruptcy protections, domestic business owners face immediate insolvency, forcing them to liquidate core assets or sell their companies entirely to avoid personal financial ruin.

Target Focus: Why Manufacturing and Packaging?

While economic distress impacts broader sectors like real estate, foreign PE funds are surgically channeling capital into Vietnam’s manufacturing and packaging industries. This targeted allocation is driven by the country’s long-term structural growth, supportive industrial policies, and highly scalable value-creation opportunities.

Packaging Industry Consolidation and the Green Transition

The Vietnamese packaging sector, valued at over USD 15 billion with projected 15-20% annual growth, is highly resilient. However, it is also extremely fragmented, comprising roughly 14,000 enterprises. A massive proportion are family-owned SMEs possessing strong client bases and modern machinery but critically lacking working capital and economies of scale. This makes the sector highly susceptible to M&A roll-up strategies.

The primary M&A catalyst is the heavily regulated transition toward green packaging. Vietnam’s Extended Producer Responsibility (EPR) mandates now require manufacturers to meet strict recycling targets or pay state contributions. For cash-strapped, highly indebted SMEs, the capital expenditure (CAPEX) required to retool for biodegradable or recycled materials is prohibitive. PE funds exploit this valuation arbitrage: they acquire distressed facilities at depressed EBITDA multiples, inject the necessary CAPEX to achieve ESG compliance, and secure premium contracts with multinational FMCG brands, rapidly multiplying the asset’s exit value.

| Sustainable Packaging Segment | Market Value / Metric | Key Growth Drivers / Legislative Support |

| Vietnam Sustainable Packaging Market | Valued at USD 1.2 Billion | Government policies; 70% of consumers willing to pay a premium; E-commerce boom. |

| Vietnam Green Packaging Market | USD 1.12 Billion (2020-2025) | Expected to reach USD 1.62 Billion by 2034 (CAGR 4.15%); EPR mandates. |

| Paper Packaging Market | USD 2.57 Billion (2024) | Reaching USD 3.59 Billion by 2034; Shift away from single-use plastics. |

| Biodegradable Alternatives | Projected 20% annual growth | Resolution 247/2025/QH15 enforcing EPR; Vietnam Ecolabel certification. |

Table 2: Vietnam’s Sustainable Packaging Market Dynamics

Manufacturing Sector Opportunities and the China Plus One Strategy

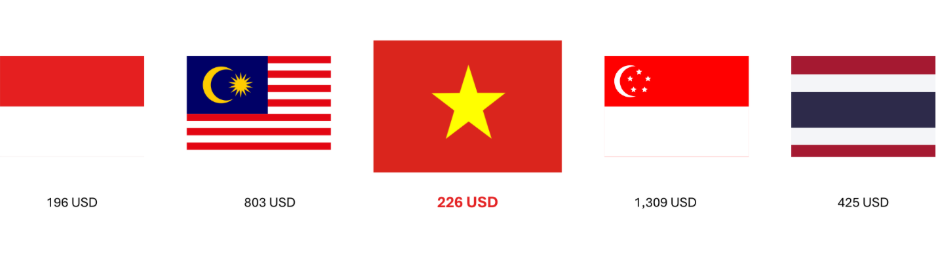

Figure 3: Average Monthly Manufacturing Wages (USD) as of 2024

Beyond packaging, the broader manufacturing sector is a strategic target due to Vietnam’s role in the “China Plus One” global supply chain realignment. While Vietnam offers competitive labor (USD 226 USD/month) and extensive Free Trade Agreements, establishing greenfield facilities from scratch is becoming increasingly expensive and bureaucratically complex.

Therefore, PE funds target distressed manufacturers to acquire hard-to-replicate core assets: long-term industrial land leases in high-occupancy zones, an existing skilled workforce, and pre-approved environmental and wastewater discharge permits. Purchasing a distressed asset with these permits already in place allows foreign investors to bypass years of bureaucratic friction.

The “Quiet Accumulation” Tactics of Foreign PE Funds

Unlike strategic corporate buyers seeking public relations value, PE funds prioritize operational stealth, employing specialized tactics to accumulate assets without triggering bidding wars.

The “Backdoor” Approach: Navigating Through NPLs

Foreign funds aggressively purchase Non-Performing Loans (NPLs) collateralized by industrial real estate from commercial banks. Now acting as the primary secured creditor, the fund leverages the threat of asset seizure to negotiate an out-of-court Debt-to-Equity swap, taking majority control while bypassing Vietnam’s slow bankruptcy courts.

The “Buy and Build” Strategy: Roll-Ups in Fragmented Sectors

In fragmented sectors, PE funds systematically acquire several smaller firms within the same value chain (e.g., a corrugated box maker, a flexible plastic producer, and a rigid container facility). Merging them into a single holding company achieves instant market dominance and powerful economies of scale. Thailand’s SCG Packaging (SCGP) exemplifies this, having quietly consolidated entities like Duy Tan Plastics (Rigid), Starprint (Offset), and SOVI (Corrugated) into a massive ecosystem.

| Acquirer | Target Company | Sector / Specialization | Deal Value / Stake | Strategic “Buy and Build” Objective |

| SCG Packaging (SCGP) | Duy Tan Plastics | Rigid Plastic Packaging | USD ~108.8M (Final 30% buyout to reach 100% control in 2024/2025) | Establish absolute dominance in the high-margin rigid packaging market and capture multinational FMCG supply chains operating in Vietnam. |

| SCG Packaging (SCGP) | Starprint Vietnam | Offset Folding Cartons | USD ~27.7M (Acquired 70% stake) | Expand aggressively into paper-based and offset packaging, diversifying the holding portfolio away from purely plastic materials to meet ESG demands. |

| SCG Packaging (SCGP) | Bien Hoa Packaging (SOVI) | Corrugated Cartons | Undisclosed (Acquired 94.11% stake) | Consolidate the essential corrugated box segment to serve heavy industrial, agricultural, and export-oriented manufacturers. |

Table 3: SCGP’s Buy-and-Build Consolidation in Vietnam’s Packaging Sector.

Injecting “Rescue Capital” and Complex Private Credit

To execute distressed acquisitions without artificially inflating asset prices or triggering regulatory scrutiny, foreign PE funds universally route capital through Special Purpose Vehicles (SPVs) in investor-friendly jurisdictions like Singapore or the Cayman Islands.

This deep corporate structuring achieves three critical strategic objectives. First, it effectively masks the Ultimate Beneficial Owner (UBO), allowing institutional players to quietly consolidate industrial sectors without alerting domestic competitors. Second, the offshore SPV framework completely bypasses time-consuming local bureaucratic hurdles. When the fund is ready to exit, the sale can be cleanly executed by transferring shares at the offshore holding company level, entirely circumventing Vietnam’s complex Department of Planning and Investment (DPI) approval process. Finally, migrating the investment structure offshore secures the transaction under predictable, common-law arbitration frameworks, effectively mitigating the legal risks associated with the evolving domestic civil court system.

Impacts on Vietnam’s Economy and Local Businesses

The influx of foreign institutional capital into Vietnam’s distressed industrial sectors acts as a profound macroeconomic double-edged sword, driving necessary market correction while threatening domestic corporate autonomy.

Opportunities for Systemic Stabilization and Modernization

On a systemic level, these interventions provide vital stabilization during a severe credit transition. By injecting rescue capital or executing comprehensive buyouts, private equity funds prevent cascading insolvencies, preserve critical manufacturing employment, and absorb toxic non-performing loans (NPLs) from the domestic banking system, thereby freeing up capital for broader economic recovery. Operationally, these acquisitions forcefully modernize the domestic industrial base. Foreign sponsors systematically replace informal, family-centric management with rigorous corporate governance, international financial reporting standards (IFRS), and advanced digital infrastructure. Crucially, they deploy the massive capital expenditure required to transition aging facilities toward strict international ESG and green production mandates, effectively subsidizing Vietnam’s continued competitiveness within highly carbon-conscious global supply chains.

Strategic Risks: Market Autonomy and Asset Stripping

Conversely, this systematic accumulation introduces severe long-term risks to the identity and control of the domestic market. The progressive absorption of legacy Vietnamese brands threatens to relegate local enterprises to highly replaceable sub-contractors, fundamentally eroding national industrial autonomy. More alarmingly, the distressed environment invites predatory special situations funds focused strictly on asset stripping. These aggressive acquirers frequently halt operations, execute mass layoffs, and liquidate highly valuable core assets—most notably long-term industrial Land Use Rights (LURs) in prime parks—for lucrative arbitrage, leaving behind hollowed-out corporate shells and unresolved systemic liabilities.

Navigating a Generational Market Purge

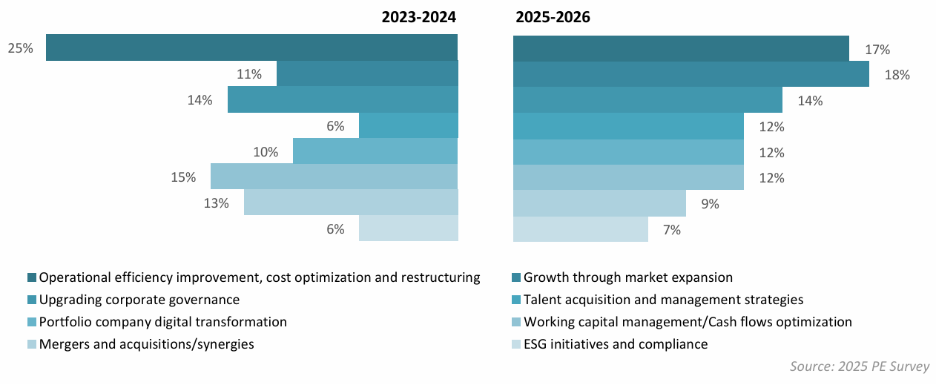

Figure 4: Value creation levers for PE investments in 2023-2024 and expected in 2025-2026

Driven by persistent domestic liquidity constraints and rigorous ESG mandates, the wave of distressed M&A across Vietnam’s manufacturing and packaging sectors is entering a transformative phase. As recent data indicates, foreign private equity funds are actively shifting their value creation playbooks; moving away from the defensive stabilization and rigorous cost optimization that characterized 2023-2024, and pivoting toward aggressive scalability, market expansion, and talent acquisition for 2025-2026.

To align with this growth-centric capital and survive the inevitable market purge, traditional SME owners must abandon their cultural insistence on absolute family control. Pragmatically embracing strategic equity sharing and institutional-grade financial transparency is now required not just to secure emergency working capital, but to fund offensive market positioning.

Ultimately, this macroeconomic convergence is facilitating a systemic wealth transfer into the optimized portfolios of foreign institutional investors. While this transition carries inherent risks of domestic brand erosion, it serves as a brutal but highly effective catalyst for industrial modernization, requiring Vietnamese entrepreneurs to utilize recapitalization to transform the immediate threat of a fire-sale takeover into a highly capitalized, growth-oriented partnership.

To explore active market opportunities, evaluate upcoming regulatory impacts, or discuss your broader Vietnam financial infrastructure thesis, connect with our advisory team at DealFlow.sg or follow our latest insights on LinkedIn.