The global energy transition is often framed as a policy-driven transformation led primarily by advanced economies. Discussions around climate regulation, carbon markets, and sustainability standards typically focus on regions such as the European Union, the United States, and Japan.

However, a closer examination of global investment patterns reveals a more complex reality. Emerging economies—particularly the BRICS nations—are increasingly shaping both the scale and trajectory of the global energy transition.

Brazil, Russia, India, China, and South Africa collectively account for roughly 45 percent of global greenhouse gas emissions and approximately 37 percent of global GDP on a purchasing-power-parity basis. Because of their industrial structures, demographic scale, and rapidly growing energy demand, policy and investment decisions within these economies will significantly influence the pace of global decarbonisation and the future direction of global energy investment.

The Scale of the BRICS Energy Transition

Growing Energy Demand in Emerging Economies

Energy demand across emerging markets continues to expand as industrialisation, urbanisation, and rising living standards drive sustained increases in electricity consumption. Unlike many advanced economies—where total energy demand has stabilised or even declined—BRICS countries must simultaneously expand their energy supply while transitioning toward lower-carbon generation sources.

This dual challenge creates a significantly more complex transition pathway. Governments and utilities must invest not only in renewable generation capacity but also in transmission networks, grid stability technologies, and energy storage systems capable of supporting intermittent power generation.

Renewable Capacity Expansion

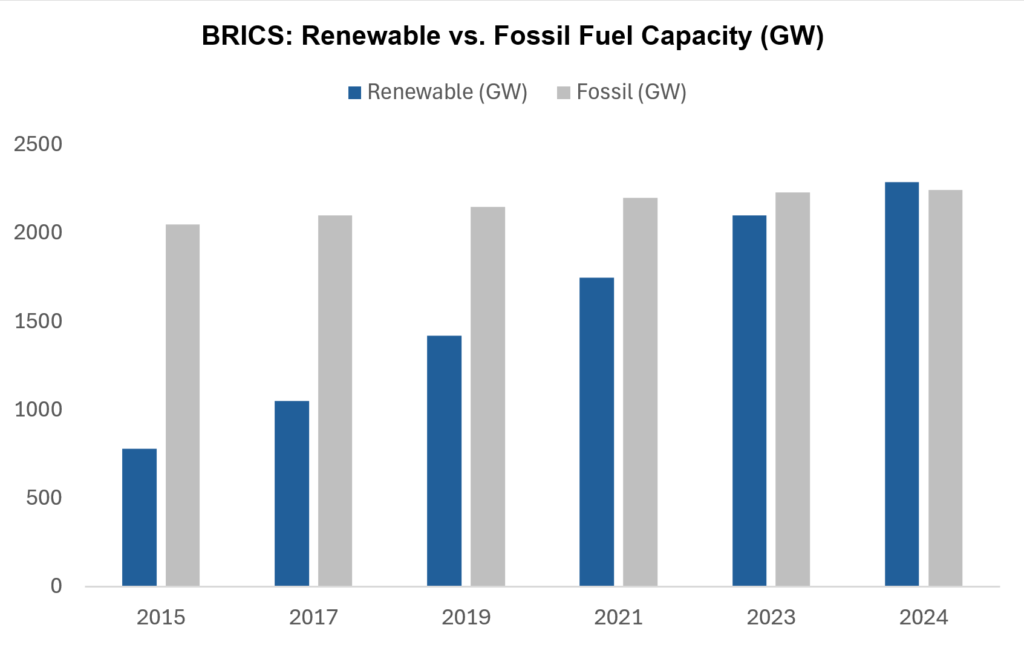

Recent data highlights the scale of this transformation. Across BRICS economies, renewable energy capacity increased dramatically over the past decade, rising from approximately 780 gigawatts in 2015 to 2,289 gigawatts in 2024.

Source: Global Energy Monitor (2025); Ember Energy (2025)

During the same period, fossil fuel generation capacity grew only modestly—from roughly 2,050 gigawatts to 2,245 gigawatts. As a result, renewable energy has steadily gained share within the region’s power generation mix.

In 2024, a symbolic milestone was reached when renewable energy capacity within BRICS economies surpassed fossil fuel capacity for the first time, representing approximately 50.5 percent of total installed generation capacity.

This shift is particularly notable given the energy-intensive structure of many BRICS economies, where industries such as steel production, heavy manufacturing, and mining remain central drivers of economic output.

Green Finance as a Catalyst for Energy Investment

Capital Requirements of Renewable Infrastructure

Financing the expansion of renewable infrastructure requires substantial long-term capital investment. Large-scale solar installations, offshore wind farms, transmission networks, and battery storage facilities typically involve significant upfront capital expenditure combined with investment horizons that can extend over several decades.

This financial structure differs from many conventional energy projects. While operating costs for renewable assets are relatively low, the majority of project costs are incurred during the initial construction phase. As a result, access to long-term and relatively low-cost financing becomes a critical determinant of project viability.

Traditional bank lending alone is often insufficient to support projects of this scale, particularly in emerging markets where domestic financial systems may have limited capacity to provide long-duration infrastructure financing. Consequently, capital markets and sustainable finance instruments have become increasingly important in mobilizing the large pools of capital required for the energy transition.

Among these instruments, green bonds have emerged as one of the most prominent financing mechanisms for climate-related infrastructure.

Expansion of Green Bond Markets in BRICS Economies

Green bonds allow governments, financial institutions, and corporations to raise capital specifically earmarked for environmental and climate-related projects while providing investors with transparent sustainability frameworks.

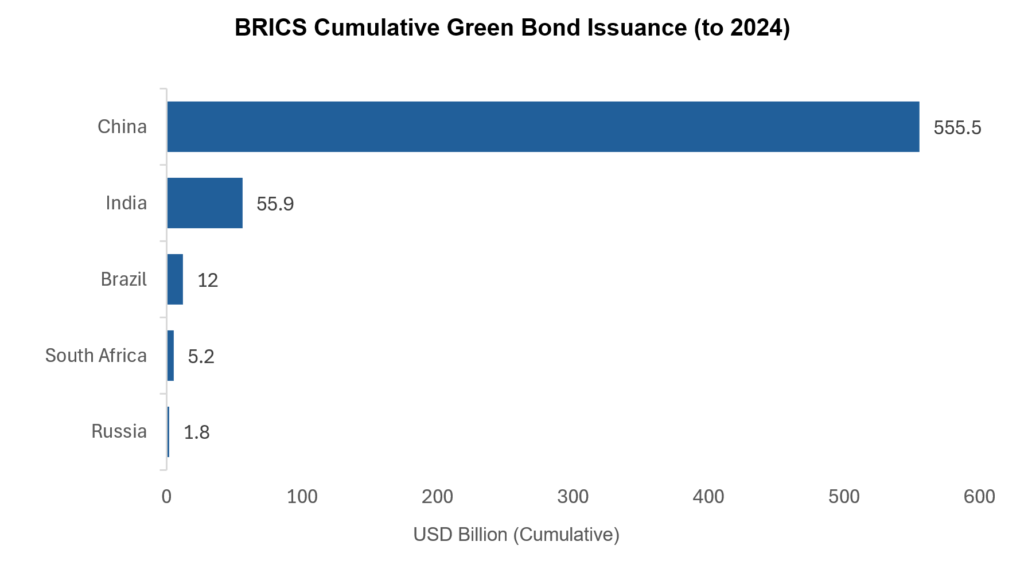

Within the BRICS bloc, China has established itself as the dominant player in sustainable capital markets. By 2024, the country’s cumulative green bond issuance had reached approximately $555.5 billion, making it the largest green bond market among emerging economies.

Source: Climate Bonds Initiative; New Development Bank (2024)

India has also begun expanding its presence in sustainable capital markets. Following the launch of its sovereign green bond program in 2023, the country has issued multiple tranches totaling roughly $5.7 billion, bringing cumulative green bond issuance to approximately $55.9 billion.

Other BRICS members have smaller but steadily developing markets. Brazil issued its first $2 billion sovereign sustainable bond in 2023, while South Africa has maintained an active municipal and corporate green bond ecosystem since the early 2010s.

Although issuance volumes vary significantly across countries, the broader trend indicates that sustainable finance instruments are becoming increasingly embedded within emerging market capital structures.

Beyond green bonds, other sustainable finance instruments are also gradually gaining traction across BRICS economies. Sustainability-linked loans, transition bonds, and climate-focused infrastructure funds are increasingly used to channel capital toward energy transition projects. As financial markets deepen and disclosure frameworks improve, these instruments may play a growing role in mobilizing long-term capital for renewable infrastructure development.

Why Emerging Markets Are Central to Global Decarbonisation

Infrastructure Expansion vs Infrastructure Replacement

The strategic importance of emerging economies in the global energy transition reflects a fundamental structural difference between developed and developing markets.

Advanced economies have already built most of their core energy infrastructure. As a result, their decarbonisation challenge largely involves replacing existing assets—such as coal-fired power plants or aging grid systems—with lower-carbon alternatives. This process is often constrained by legacy infrastructure, regulatory complexity, and the high costs associated with retiring or retrofitting existing systems.

In contrast, many emerging economies are still expanding their energy infrastructure to meet rapidly growing electricity demand. This creates a distinct structural advantage: new power systems can be designed around renewable technologies from the outset rather than retrofitting legacy infrastructure. As a result, a significant share of future energy investment in these markets may flow directly into low-carbon generation, transmission networks, and grid-scale storage systems.

From a capital allocation perspective, this distinction is critical. While developed economies focus primarily on asset replacement, emerging markets are simultaneously building new energy capacity and shaping the long-term architecture of their power systems—making them a central arena for global renewable infrastructure investment.

Accelerating Renewable Deployment

The pace of renewable deployment across BRICS economies illustrates this structural advantage. In 2023 alone, wind and solar power accounted for approximately 98 percent of renewable capacity growth within the bloc, adding around 331 gigawatts of new capacity in a single year.

Looking ahead, projections suggest that renewable energy capacity within BRICS economies could nearly triple by 2030, potentially reaching more than 5,400 gigawatts.

Such expansion would significantly accelerate global progress toward long-term decarbonisation targets. Given the scale of future energy demand across emerging economies, a substantial share of global renewable investment over the coming decades is likely to be directed toward these markets. However, achieving this outcome will require continued mobilisation of large-scale investment from both domestic and international capital markets.

Investment Implications for Global Capital Markets

Risks and Structural Constraints

For investors, the growing role of emerging economies in the global energy transition presents a complex balance between opportunity and structural risk.

Emerging markets often face institutional and financial constraints that can complicate the financing of large-scale renewable infrastructure projects. Regulatory frameworks may evolve rapidly as governments adjust energy policies, tariff mechanisms, and market structures in response to shifting economic conditions. Such policy uncertainty can affect long-term project economics, particularly for renewable assets that typically require investment horizons of twenty to thirty years.

Currency volatility also represents a significant challenge for international investors. Renewable infrastructure projects in emerging markets frequently generate revenues in local currencies, while a large portion of project financing—particularly from international lenders and development finance institutions—is denominated in major global currencies such as the US dollar or euro. This mismatch can introduce additional financial risk, particularly during periods of macroeconomic instability or capital market stress.

Financial market depth is another structural constraint. Compared with advanced economies, many emerging markets still have relatively underdeveloped long-term capital markets capable of supporting large-scale infrastructure financing. Limited availability of long-duration debt instruments, higher borrowing costs, and smaller institutional investor bases can increase the cost of capital for renewable projects even when underlying resource potential is strong.

As a result, renewable energy investment in emerging markets often relies on complex financing structures that combine domestic bank lending, multilateral development finance, export credit agencies, and international institutional capital. While such blended financing models can mobilize substantial capital, they also increase transaction complexity and extend project development timelines.

Long-Term Growth Opportunities

Despite these structural challenges, emerging markets represent some of the most significant long-term growth opportunities in global renewable energy deployment.

Many BRICS economies possess natural resource advantages that support large-scale renewable generation. Solar irradiation levels in regions such as India and Brazil rank among the highest globally, enabling highly competitive solar generation costs. At the same time, China has developed a globally dominant manufacturing ecosystem for renewable technologies, producing a substantial share of the world’s solar panels, wind turbines, and battery components. This industrial capacity not only supports domestic deployment but also shapes global supply chains for clean energy infrastructure.

The scale of future energy demand further amplifies the investment opportunity. Rapid urbanisation, population growth, and industrial expansion across emerging economies will require significant increases in electricity generation capacity over the coming decades. Unlike many advanced economies where energy infrastructure is largely mature, these markets must build substantial new capacity, creating long-term demand for renewable energy investment.

As sustainable finance frameworks mature and regulatory environments gradually stabilise, international capital flows toward emerging market renewable infrastructure are likely to accelerate. Institutional investors—including pension funds, sovereign wealth funds, and infrastructure funds—are increasingly seeking long-duration assets capable of generating stable, inflation-linked returns.

Within this context, green finance instruments such as green bonds, sustainability-linked loans, and climate-focused infrastructure funds provide structured channels through which global capital markets can participate in emerging market energy transition projects.

Key Takeaways

The global energy transition is no longer driven solely by advanced economies. Emerging markets—particularly the BRICS nations—are playing an increasingly central role in shaping the scale and trajectory of global decarbonisation. Rapid expansion in renewable energy capacity, combined with the growing adoption of sustainable finance instruments, suggests that these economies are becoming key destinations for climate-related capital deployment.

For policymakers, the priority lies in developing regulatory and financial frameworks capable of supporting large-scale sustainable investment. For investors, the opportunity lies in participating in one of the most significant infrastructure transformations in modern economic history. As renewable deployment accelerates and capital markets deepen, the intersection of green finance and emerging market energy investment will likely remain a defining theme in global capital allocation.

For deeper insights on capital markets, infrastructure investment, and emerging market opportunities, follow Dealflow for research-driven perspectives on global finance via LinkedIn or explore further analysis at Dealflow.sg.