Vietnam’s economic resilience continues to fuel a profound shift in domestic consumption, specifically pivoting toward experiential travel and premium leisure. The expansion of the middle and mass-affluent classes is a visible economic force driving the domestic resort market, which recorded 137 million trips in 2025. This domestic baseline provides critical cash-flow stability for coastal assets.

Post-China Inbound Diversification

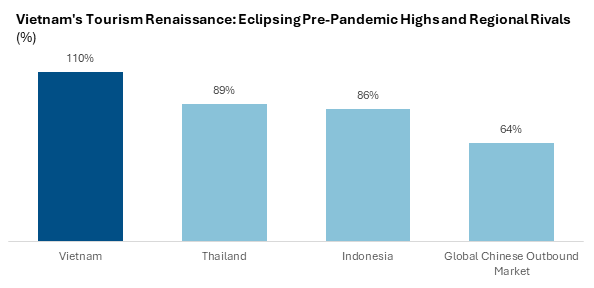

In the context of ASEAN tourism, Vietnam has successfully disrupted the traditional hierarchy. By welcoming more than 22 million visitors in 2025, it achieved a recovery rate of 110% compared to the 2019 baseline, significantly outperforming Thailand (89%) and Indonesia (86%). This ascent reflects a successful diversification strategy that has mitigated the slower recovery of the Chinese outbound market—which remains at roughly 64% of pre-pandemic levels globally—by cultivating high-growth corridors in South Korea, India, and Europe specifically seeking premium coastal and wellness experiences.

Figure 1: Tourism Recovery Rates vs. 2019 Baseline

The composition of Vietnam’s inbound traffic has shifted, reducing concentration risk for resort owners. South Korea remains the volume anchor, contributing nearly 490,000 arrivals in January 2026 alone, creating a stable “base load” of demand for mid-to-luxury beachfront assets in Central Vietnam. Simultaneously, India has emerged as the growth engine, with arrivals surging 80.5% year-on-year. This demographic is proving critical for the luxury wedding segment and MICE, often booking entire resorts for multi-day events during shoulder seasons, thereby smoothing occupancy curves. Furthermore, following the expansion of visa waivers to 12 additional European nations in late 2025, European arrivals grew by 35% in early 2026, reinforcing the high-yield, long-stay segment essential for coastal integrated resorts.

Valuation Drivers: How Logistics & The ‘Long Thanh Effect’ Are Re-Rating Coastal Land Banks

The most tangible driver of asset appreciation in Vietnam’s resort sector is the physical transformation of the country’s transport logistics. The market is currently witnessing the peak delivery phase of a decade-long infrastructure super-cycle, which is fundamentally altering the distance-to-value equation for leisure real estate.

Aviation Capacity and the LTIA Gateway

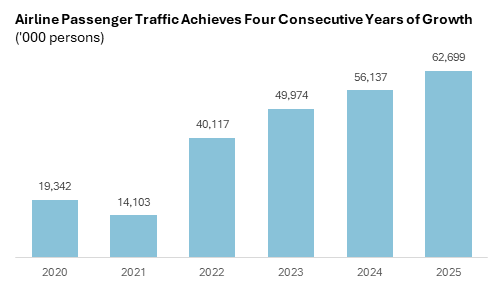

The Long Thanh International Airport (LTIA) represents the single most significant infrastructure project for the southern leisure corridor. With Phase 1 commercial operations confirmed for H1 2026, the airport adds capacity for 25 million passengers annually, alleviating the chronic congestion at Tan Son Nhat (SGN). For investors, LTIA changes the gravity of the resort market. It serves as a direct gateway to the south-central coast—specifically Ho Tram and Phan Thiet—allowing international traffic to bypass urban gridlock. This structural shift is actively re-rating land values in these satellite destinations as they become accessible within 90 minutes of landing.

Figure 2: Passengers Carried 2020-2025 (Euromonitor, 2025)

The “Drive-To” Expressway Network

Parallel to aviation, the completion of critical sections of the North-South Expressway (CT.01) is converting isolated “fly-to” beaches into accessible “drive-to” weekend getaways. The reduction of drive times—HCMC to Nha Trang under 4 hours, and HCMC to Phan Thiet under 2.5 hours—enables a true “52-week” resort economy. For owners, this connectivity reduces reliance on flight schedules, allowing robust weekend domestic occupancy to subsidize lower mid-week international demand. This dynamic stabilizes cash flows and significantly improves debt service coverage ratios (DSCR) for assets located within the expressway corridor.

The Regulatory Moat: Land Law 2024 and the Formalization of Resort Tenure

The implementation of the Land Law 2024 (Law No. 31/2024/QH15), effective January 1, 2025, represents a paradigm shift for resort investment. It moves the market from a “grey area” of quasi-ownership to a codified system of rights and obligations, specifically addressing the “condotel” and resort villa models that were previously plagued by legal uncertainty.

Codifying Asset Tenure

The new law, supported by Decree 10/2023, explicitly authorizes the issuance of Land Use Right Certificates (Pink Books) for construction works built on commercial/service land used for tourism accommodation. Ownership is granted for a definite term—typically 50 years, extendable to 70 years in economic zones. While distinct from residential land, the certainty of the title allows for mortgageability, transferability, and inheritance, which are crucial mechanisms for unlocking secondary market liquidity for resort developers.

Market-Driven Land Pricing

However, the law also introduces higher barriers to entry. The abolition of the government’s 5-year land price frame in favor of annual land price tables determined by market principles means land use fees will now track market value more closely. This significantly increases the upfront capital requirement (Capex) for new coastal projects. Consequently, higher land costs will erode the margins of mass-market budget developments, effectively pushing developers toward luxury and ultra-luxury segments where high Average Daily Rates (ADR) can justify the increased land basis. This regulatory change favors well-capitalized institutional developers over smaller speculative players.

Asset Class Mechanics: Yield Compression & The Rise of the ‘Manachise’ Model

Operationally, the resort market is rapidly evolving from owner-operated properties to professional third-party management and franchising.

The Institutional “Manachise” Shift

The increasing complexity of digital distribution, revenue management, and the need for global loyalty program access is compelling owners to partner with global hospitality chains. Chain hotel inventory is forecast to grow at an 11.65% CAGR through 2031, exemplified by Masterise Group’s partnership with Marriott International. This operational institutionalization is driving a projected 6% growth in Gross Operating Profit (GOP) for Vietnam in 2026.

Monetizing the Captive Guest Ecosystem

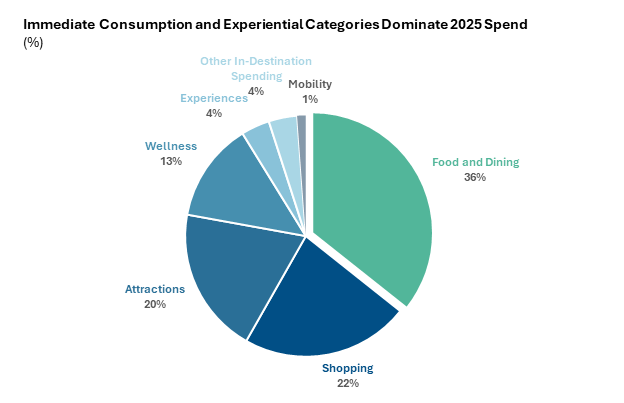

Figure 3: Estimation of In-destination Spending in 2025 (Euromonitor, 2025)

The 2025 in-destination spending profile mandates a radical rethink of asset underwriting in Vietnam’s hospitality sector. With Food and Dining (118,326.4 VND billion) and Wellness (44,251.0 VND billion, driven exclusively by the spa segment) representing a disproportionate share of the total expenditure, these components can no longer be modeled as secondary amenities; they are the primary engines of Gross Operating Profit (GOP).

More critically, the transaction velocity is overwhelmingly spontaneous and on-premise. The data reveals a massive structural reliance on direct offline transactions, which captured 239,781.4 VND billion—dwarfing the entire online booking ecosystem. For institutional investors and operators, this dictates a clear strategic imperative: the true alpha lies in “wallet capture” post-arrival. Assets that deploy frictionless, on-property digital ecosystems and high-conversion experiential upselling will achieve superior yield and valuation premiums, successfully monetizing the captive guest while legacy competitors merely rent them a room.

Geographic Arbitrage: Identifying Mispriced Resort Micro-Markets

Investors must adopt a granular, location-specific strategy, as Vietnam comprises distinct coastal and leisure micro-markets with varying risk-return profiles.

| Micro-Market | Investment Theme | Key Strengths & Catalysts | Primary Risks & Constraints |

| Phu Quoc | The Sovereign Bet | 2027 APEC Summit infrastructure upgrades; entry of top-tier luxury brands. | Oversupply in the mid-market shophouse segment. |

| Van Don | The Gaming Anchor | $2B casino complex; proximity to cross-border expressways; potential domestic gambling pilot. | High-beta risk heavily reliant on the success of the regulatory gambling pilot. |

| The “New” Coast (Quy Nhon, Phu Yen, Cam Ranh) | Infrastructure Arbitrage | Primary beneficiaries of the expressway; lower entry prices with identical natural endowments. | Early-stage development risk requiring longer-term land banking and master-planning. |

Table 1: Strategic Risk-Return Matrix by Resort Micro-Market

Risk Vectors: The Human Capital Crunch & Capex Inflation

While the macro story is bullish, the micro-operational environment for resorts presents acute challenges.

Talent Deficits and Rising Costs

The most severe risk in 2026 is the human capital crisis. Rapid coastal supply expansion has completely outpaced workforce development, with 67% of hospitality businesses reporting severe hiring difficulties. Wage inflation for skilled, English-speaking staff is expected to rise 30-40%, forcing investors to model higher payroll costs and prioritize internal training academies.

Additionally, construction inflation driven by global tariffs and the new Land Law’s impact on acquisition costs means the era of “cheap land, cheap labor” is over. Development feasibility now relies entirely on premium positioning and operational excellence.

DealFlow Perspective: Executing in a High-Velocity Market

Vietnam’s resort sector in 2026 offers distinct alpha for strategic capital, but the window for acquiring prime coastal assets at distressed valuations is closing. The market has bifurcated: “easy beta” is diminishing, replaced by returns generated through superior deal structuring, rigorous due diligence, and operational value-add.

As a specialized M&A and fundraising advisory firm, we do not merely track the market—we facilitate the transaction. Whether you are a buy-side fund seeking off-market beachfront assets with clean tenure, or a developer looking to raise capital and divest non-core leisure holdings, our team provides the on-the-ground intelligence required to navigate Vietnam’s opaque regulatory and valuation landscape.

To discuss your strategic investment criteria and operationalize your Vietnam thesis, connect with our advisory team at DealFlow.sg or follow our latest insights on LinkedIn.